Immunochemistry Instruments and Reagents

Immunochemistry market is now back to normal

Improvements in assay design, Ab structure and specificity, and signal generation and detection, with an increasing number of assays, developed to detect more molecules, have made immunoassays one of the most used techniques in clinical laboratories. However, there has also been a trend to simplify methods to facilitate automation, and new innovative therapies result in new interferences.

Some of the major specificity problems in competitive assays are related to the measurement of steroids and structurally related compounds. Therefore, many laboratories have started using LC-MS/MS for the quantification of these analytes, although these methods are more expensive and technically demanding than immunoassays. LC-MS/MS avoids main specificity problems, and also provides multi-parameter quantification in the same analytical session, allowing for steroid profiles to be generated with a dramatically reduced sample volume, which is valuable for newborns and infants.

Unfortunately, these powerful and reliable measurements are not yet adapted to high-throughput sandwich assays. As protein and macromolecule assays with LC-MS/MS become more amenable, the use of immunoassay-based measurements may decline to improve specificity and robustness with respect to immunological interference, notably for some critical assays, such as Tg as a major biomarker for the follow-up and management of differentiated thyroid cancer. While waiting for these improvements, immunoassays, despite their drawbacks, will still be in general use, at least for a few years, and the problem of immunoassay interference will persist.

Laboratory knowledge plays a central role in highlighting possible interference. When a clinician deals with unexpected or incoherent results regarding patient conditions, a strong interface with laboratory specialists facilitates the rapid identification of incoherent results. Informing the clinical staff of the ever-present possibility of unexpected sporadic interference, notably from an endogenous Ab, is needed.

When facing unknown interference, which might require more deep and specialized investigations, feedback from laboratory to manufacturers enables the manufacturers to actively search for a solution to the emerging problem and to keep improving the immunoassay robustness with respect to the risk of interference. Granting laboratory specialists access to the clinical and therapeutic records of patients is important, when they suspect and try to detect interference.

Specifically, the notion of biotin or a specific therapy has become a key question. In addition, the notion of previously administrated immunotherapies must always draw the attention of laboratory specialists to the possibility of Ab-induced interference in immunoassays. Ideally, an interfering therapy should automatically be flagged; thus, minimizing interference risk can also be achieved by connections between health information systems and laboratory information systems.

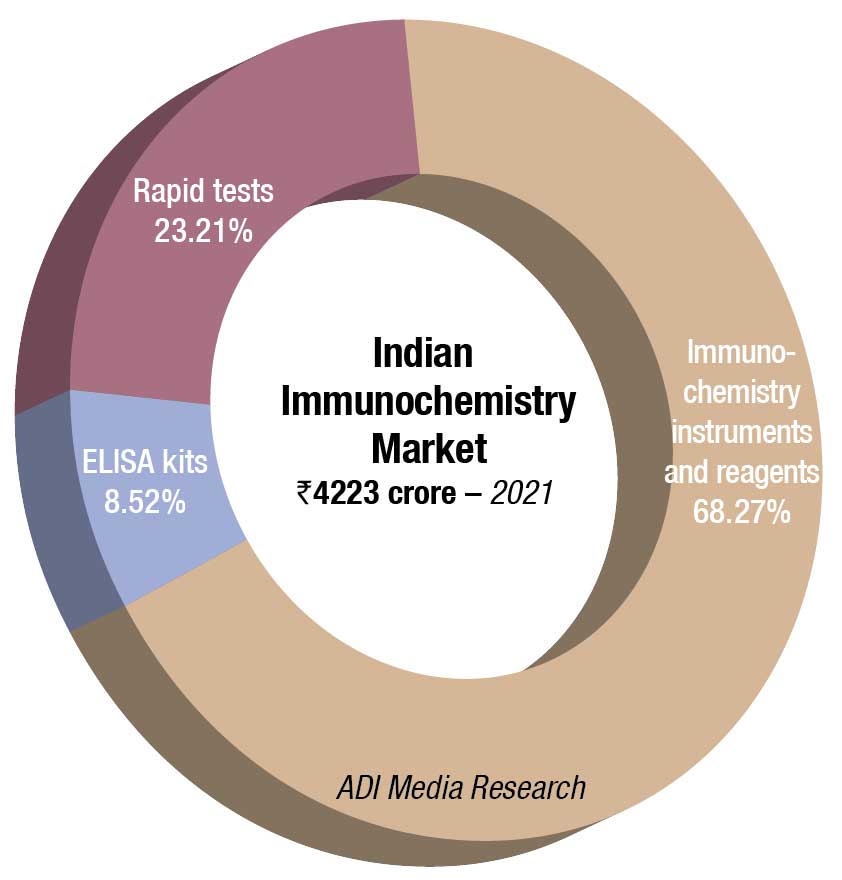

The Indian immunochemistry instruments and reagents market in 2021 is estimated at ₹2883 crore. Reagents continue to dominate the segment at ₹2645 crore. Additionally, the rapid tests’ market clocked ₹980 crore, with dengue and Covid assays being the major ones. The ELISA market is estimated at ₹360 crore. With blood banks being closed for a long time, and fewer blood camps held, these tests received a setback.

While routine immunochemistry and infectious disease testing declined, laboratory biomarkers, serum C-reactive protein (CRP), procalcitonin (PCT), D-dimer, and serum ferritin became essential to forecast the severity of the pandemic. Serosurveys, considered an important tool to map the trajectory of the pandemic, conducted at public hospitals, resulted in huge tenders and bulk buying.

|

Major vendors* in immunochemistry instruments and reagents market

|

|

| Tier I | Roche |

| Tier II | Abbott |

| Tier III | Beckman Coulter, and OCD |

| Tier IV | bioMérieux, Transasia, Mindray, and Agappe |

| Others | Tosho, Bio-Rad, Maglumi ( SNIBE and Immunoshop), and CPC |

| *Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian immunochemistry instruments and reagents. | |

| ADI Media Research | |

A serosurvey is a population-wide sampling test done over a fixed period of time. It is traditionally done by taking blood samples from a random selection of people across ages and regions, to look for antibodies against SARS-CoV-2 – the virus that causes Covid-19. The results, which indicate how much of the population is/was likely infected and how many have recovered, can help shape strategic decisions around the pandemic.

Four rounds of Covid-19 national serosurveys have been conducted by the ICMR (Indian Council of Medical Research) so far, the first one between May 11 and June 4, 2020, and the fourth one between June 14 and July 6, 2021.

It is only from the fourth quarter, Oct 2021 onwards, that normalcy returned. Since there was no shortage of kits, the organized segment, the MNCs, saw 20 percent increased sales in 2021, over 2020. And April 2022 onwards, it is expected that serology testing will once again take a backseat. 2022 is expected to report a 10–12 percent growth, per annum.

The global immunoassays market is expected to reach USD 46.49 billion by 2028, at a CAGR of 7.5 percent during 2022–2028. Compared to conventional tests, immunoassays have been proven to provide highly accurate results even with very small samples. These immunoassays are considered to have a detection limit of 1 pg/mL, which can be attributed to the fact that immunoassays are based entirely on immunologic reactions. Immunologic reactions are highly specific, as they can take place only in the presence of proper immunologic agents. For instance, an antibody against a viral protein cannot bind with an antigen that is derived from bacteria. This high specificity indicates high accuracy in results, which enables high sensitivity in the detection of diseases. This high sensitivity not only helps in easy detection but also eliminates the need for secondary verifications, which ultimately saves a lot of costs. Thus, the high-sensitivity, specificity, and cost-saving nature of immunoassays is driving the growth of the immunoassays market.

In the absence of vaccine or specific therapy, diagnosis is the only way to control and manage the wide spreading of infectious disease, and immunoassays played this role significantly in curbing the spread of recent global pandemic condition of Covid-19. The massive research, validations, and approvals of several immunoassay consumables and analyzers have alleviated the issue of SARS CoV2 detection. There has been a surge in use of immunoassays, such as chemiluminescence, ELISA, and lateral flow base point-of-care (POC) rapid test.

Despite the long history of immunoassay IVD kits and reagents and maturity of the field, companies continue to develop new immunoassays and instrument platforms to improve assay sensitivity. New developments, expanding the future potential of immunoassays, include making multiplexing possible, miniaturizing platforms for POC testing, and identifying and developing assays for novel biomarkers.

The immunoassays market is large and, in some areas, locked up by large IVD companies, but there is a plenty of opportunity for innovators and for niche players developing antibody or antigen-based tests. Some of the leading players include Abbott, SNIBE Diagnostic, Thermo Fisher Scientific, Sysmex Corporation, Beckman Coulter, bioMérieux, Roche Diagnostics, Bio-Rad, Siemens Healthineers, Radiometer, DiaSorin, Fujirebio, and Ortho Clinical. More than 100 other companies compete for market share in immunoassays, while smaller players with ELISA tests serve local markets. Strong niche competitors, including Thermo Fisher Scientific, bioMérieux, Sysmex Corporation, DiaSorin, and Wako, market their products worldwide. Other smaller companies have experienced remarkable growth, but their total revenues contribute only a small portion of the total market.

With the rising need for one system to handle a high number of samples for biochemistry, immunoassay, and electrolyte assays, integrated systems of biochemistry, CLIA, and electrolyte modules are appealing in large-scale laboratories. Research and development of CLIA systems that can integrate with other modules and have a bigger test menu are being driven by the growing demand for complex integrated systems in the IVD industry.