Immunochemistry Instruments and Reagents

Indian immunochemistry market plummeted in 2020

The Indian immunochemistry analyzers and reagents market, sans the COVID-19 rapid antigen tests, saw a 22 percent decline. The immunochemistry analyzers had just begun to replace clinical chemistry and immunoassay as new or improved assays were being added to the test menus incrementally. Moving forward, the Indian market in 2021 is expected to see a 25-30 percent increase over the 2019 sales figures.

Immunochemistry analyzers are becoming more and more standard within the world clinical chemistry and immunoassay as these are proven to be an amazingly effective tool to diagnose cancer, hepatitis, illegal drugs, fertility issues, sodium levels, endocrine function, and the detection of blood clots. Use of immunoassays and other ligand-binding assays in clinical diagnosis has increased dramatically during the last several years.

There have been tremendous advances in IVD assays for coronavirus disease caused by severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2). Two general methods are used in the diagnostic detection of COVID-19: the sequence-specific molecular nucleic acid test and the antigen-specific immunoassay. These techniques are the current gold standards for diagnosing acute infection and for monitoring immune response. There are now over 70 COVID-19 diagnostic tests that have been authorized for emergency use by the USFDA. The vast majority are molecular assays, while approximately one-fifth are antibody immunoassays.

Chemiluminescence immunoassays (CLIA) are quantitative serological antibody detection assays, which have high sensitivity and specificity. The enzyme-linked immunosorbent assay (ELISA) uses enzyme-substrate reactions to produce measurable signals proportional to the concentration of the target analyte. A defining feature of the ELISA is the immobilization of the target antigen upon a solid surface, usually in microplate wells. ELISA kits are sensitive, quantitative tests that can be used to measure a variety of analyte types within complex samples. Compared to the ELISA, lateral flow assays are generally qualitative, rather than quantitative. However, the relative simplicity of the procedure has led to the widespread development of various point-of-care and direct-to-consumer devices. Many tools are available that make it possible to run immunoassay experiments or even develop new, customized tests. At the heart of the assay are specific SARS-CoV-2 antibodies for targeting various antigens. Recombinant SARS-CoV-2 proteins can be used to develop controls or targets or to serve as antigens for immunoglobulins.

In the current COVID-19 pandemic, ELISA tests are playing a key role in testing, surveillance, and epidemiological studies. A typical ELISA protocol entails multistep manual operations that at some point become challenging from an operational and compliance perspective. The last two decades have seen tremendous innovation in ELISA technology. Automated ELISA processors are equipped with robotic probes and dedicated workstations, which drastically improve ELISA workflows, in terms of technology, features, accuracy, and cost-effectiveness.

Market driven specific protein systems

Sanjaymon KR

Sanjaymon KR

GM-Business Development, Agappe Diagnostics

The pandemic has changed many equations in the IVD industry. It was an eye opener to manufacturers around the world. There is an exponential growth in molecular diagnostics-based testing. similarly, parameters like Immunoglobulins, PCT, D-Dimer, CRP, and Ferritin used as a prognosis tool for COVID contributed the growth in the immunochemistry segment.

The IVD industry witnessed introduction of innovative solutions especially in the specific protein market. Procalcitonin (PCT) which is used as a sepsis marker was available earlier in CLIA based or IFA based platform which is highly priced eluding laboratories in tier-III cities. Agappe being the forerunner in the specific protein market was successful in introducing procalcitonin in our cartridge based specific protein system Mispa -i3. Today Agappe is the only IVD manufacturer in India to have Procalcitonin, D-Dimer, CRP, and Ferritin in specific protein system. We are planning to have more and more inflammatory markers in the specific protein platforms to make it one of the unique products globally. We are also in the verge of introducing a fully automated compact cartridge based clinical chemistry and specific protein system to address the market needs.

It is estimated that the installation base of specific protein systems in India will cross the 10,000 mark in the financial year 2021 and owing to the increase in the installation base, the specific protein-based tests conducted in India will cross 100,000 tests per day mark by end of FY21. It is expected that the specific protein market will grow at 28 percent for the coming 3 years and will become one of the major contributors in the immunochemistry segment. It is also expected that more and more parameters are going to be added in the specific protein segment, which will make affordable diagnosis for the masses in India and the nearby developing countries.

A range of automated ELISA processors are available for all kinds of workloads and spatial setups – from a compact bench-top ELISA strip processor to 1-, 2- 3-, 4- or 6-microplate processors.

These fully automated ELISA processors are complete walk-away systems that minimize manual errors, while improving accuracy and turnaround time for critical tests. Usually being open systems, the limitation of ELISA kits from a single source, can also be ruled out.

Companies in the immunochemistry diagnostic devices and equipment market are increasingly investing in automated immunoassay systems. This is mainly because automation has led to an increase in the capabilities of diagnostic devices in testing higher volumes of patient specimens. In addition, the development of various integrated clinical chemistry systems has immensely improved the efficiency of the analytical phase of clinical chemistry laboratory testing and led to further automation.

In addition, ongoing global efforts are working to communicate and facilitate new diagnostic assay development and worldwide test kit delivery. To promote more accurate and faster diagnostic solutions, a number of organizations are supporting these efforts by inviting assay developers to submit their test products for independent evaluation or by providing huge investments for greater collaboration.

As similar initiatives and knowledge sharing become available, including collaborative technological advancements, it is likely that the immunochemistry market will continue to thrive well into the future.

Indian market

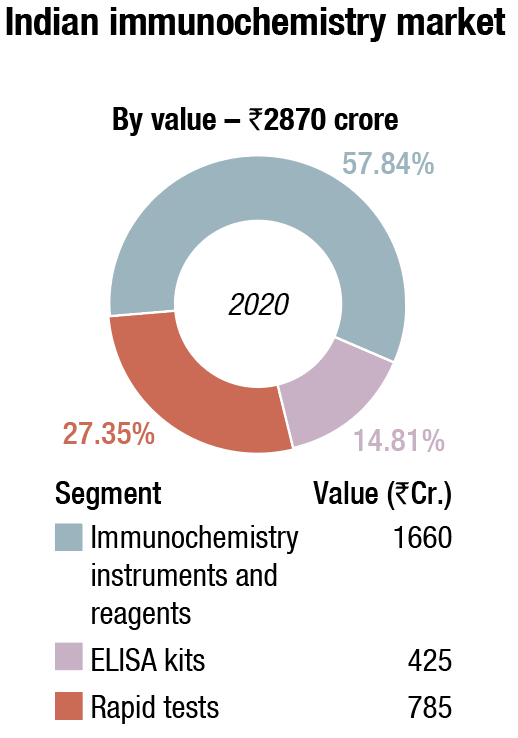

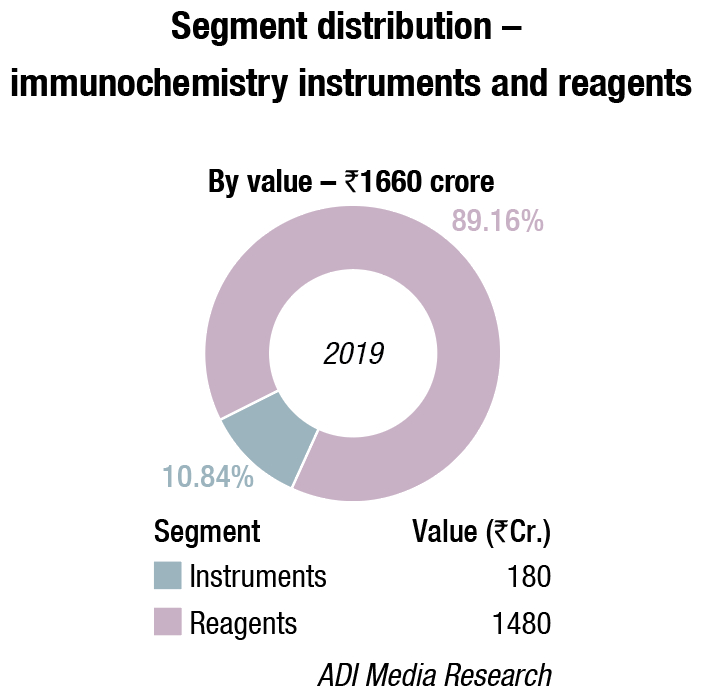

The Indian immunochemistry instruments and reagents market, in 2020, sans the COVID-19 rapid antigen tests is estimated at ₹1660 crore, a significant drop from ₹1912 crore in 2019. Reagents continue to dominate the segment, with an 89 percent share at ₹1480 crore.

The 22 percent decline, with the setback from COVID, hit the entire industry. There was some respite from the antibody tests conducted, but they only picked up pace later in the year. The serosurveys, conducted on a large number of people, by the government in several parts of India testing the presence of antibodies led to demand for the product.

In fact, the first quarter of 2021 has also been slow. It is only in May that the industry began to see some momentum. The government and the private sector started placing orders again, with a distinct bend toward automation. The incidence of COVID-19 has changed the mindset and now all laboratories have automation high on the agenda. However, with mandatory accreditation still not enforceable, the unorganized segment continues to thrive and with it the inefficiencies in the system.

Roche dominates this market, followed by Abbott, and Siemens, each at a 12-13 percent market share. Beckman Coulter and OCD are at around a 10 percent share, with bioMérieux estimated around 7 percent. Agappe, Transasia, and Mindray are also aggressive.

The market in 2021 is expected to see a 25-30 percent increase over the 2019 sales figures.

| Major vendors* in immunochemistry instruments and reagents market – 2020 |

|

| Tier I | Roche |

| Tier II | Abbott and Siemens |

| Tier III | Beckman Coulter and OCD |

| Tier IV | bioMérieux, Transasia, Mindray, and Agappe |

| Others | Tosho, Bio-Rad, Maglumi (SNIBE and Immunoshop), and CPC |

| *Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian immunochemistry instruments and reagents market. | |

| ADI Media Research | |

An increase in the incidence of target diseases is a major driver for the immunochemistry instrument and reagents market. The incidence rate of diseases such as viral infections, cardiovascular diseases, cancer, or hormonal disorders is increasing worldwide, mainly due to poor lifestyle choices. There is a rising focus on biomarker development across the globe as they help in detection of various diseases in their initial stage. Immunochemistry plays a crucial role in the development of biomarkers thus with the growing demand of biomarkers, the market for immunochemistry instruments and reagents will also flourish. Furthermore, government support in terms of funds and grants has also provided much needed impetus to this market. Moreover, increasing focus on drug monitoring and growing incidences of various diseases are other factors driving the growth of the market. In addition to this, technological advancements due to which automated and more accurate instruments are present in the market is another major factor propelling the growth of the market.

Global market

The global immunochemistry instrument and reagents market is expected to grow from USD 15.01 billion in 2020 to USD 16.49 billion in 2021 at a compound annual growth rate (CAGR) of 9.9 percent, estimates The Business Research Company. The change in growth trend is mainly due to the companies stabilizing their output after catering to the demand that grew exponentially during the COVID-19 pandemic in 2020. The market is expected to reach USD 20.36 billion in 2025 at a CAGR of 5.4 percent.

Automation in ELISA greatly enhances workflow

Rajendra Margam

Rajendra Margam

Sr Product Manager – Immunology, Transasia Bio-Medicals Ltd.

Enzyme-linked immune sorbent assay (ELISA) is a highly sensitive and selective analytical technique that is commonly used to detect the presence of a specific protein (antigen or antibody) in blood samples. Whether a lab works with direct, indirect, sandwich or competitive assays, ELISA protocols involve an exhausting number of dispensing, washing and incubating steps. However, this continues to remain the most widely used microplate assay in diagnostics and research.

The automation of ELISA systems, in the recent past, has further contributed to improving the turnaround time for critical tests.

Need for automation

In the wake of the increasing need to conduct different assays for infectious disease and hormone panels, management of multiple ELISA protocols manually, can be time-consuming. This is where automation of ELISA protocols plays a role in ensuring reliability and consistency in:

-

Time and temperature of incubation;

-

Reproducibility of washing process to avoid carry-over of sample and reagents; and

-

Simultaneous and sequential dispensing through robotic probes.

Besides this, most automated ELISA processors are open systems, allowing flexibility and greater degree of accommodation in expanding the test menu. Most importantly, automation helps in improving workflow efficiency by freeing the laboratory staff from repetitive steps. In fact, automation greatly improves the quality of data generated. It has been noted that on a standardized and validated automated system, replicates on a plate as well as across the plates, show lower co-efficient of variation (CV) when compared to a manual system.

Choosing the right ELISA automation for your lab

In order to gain maximum from automation, one should determine the scale and scope of automation, based on the lab requirement and choose an instrument accordingly. Thoughtful planning and careful implementation, based on test menu, workload and lab infrastructure, can determine the overall success of automating the ELISA process.

Automation can be implemented on the simplest assay format like an ELISA plate reader to a high capacity, modular 6-plate processors for multiple parameters. Transasia Bio-Medicals offers a complete range of fully automated 2½ and six plate ELISA microprocessors for a wide range of infectious diseases and hormone assays.

Stringent regulatory policies related to approval of immunoassay instruments and consumables are major restraints for the immunochemistry diagnostic devices and equipment market.

Immunochemistry devices and equipment manufacturers are required to obtain multiple and separate clearances from the Food and Drug Administration (FDA) for launching their products. The entire process of regulatory approval is time-consuming, with a minimum of about 18-30 months required for approval of class III devices and around 6-9 months required for approval of class II devices.

In the USA, the immunochemistry diagnostic devices and equipment market is regulated under the US Food and Drug Administration (FDA), and all diagnostic laboratory tests are regulated by the clinical laboratory improvement amendments of 1988 (CLIA), which is administered by the Centers for Medicare & Medicaid Services (CMS). A CLIA/FDA compliant laboratory is required to file a PMA/510(k) for market approval of any immunochemistry device. Hence, the regulatory scenario related to immunochemistry diagnostic devices and equipment will keep a check on the companies that manufacture these devices and equipment.

Under the robust rules and regulation laboratories notice it difficult to have good revenues. Therefore, it is vital to seek out ways to sustain in such a cost-crunched environment. Thanks to the price cutting in clinical lab fees, profit per check is decreasing that makes it necessary for the laboratories to focus on the volume instead of the worth. There is additionally significant pressure for quality, error-free results to ensure patient satisfaction. This forces labs to lean toward a lot of automated systems with effective workflow solutions.

Thermo Fisher Scientific, Siemens Healthcare, Roche Diagnostics, Abbott Diagnostics, Beckman Coulter, Danaher, Ortho Clinical Diagnostics, and others are among the major players in the global immunochemistry analyzers market. The companies are involved in several growth and expansion strategies to gain a competitive advantage. Industry participants also follow value chain integration with business operations in multiple stages of the value chain.

Dr Pramod Ingale

Dr Pramod Ingale

Professor and Head, Dept. of Biochemistry, LTM Medical College and LTMG Hospital

“Ongoing technological innovations have made immunoassay tests available and affordable to common individuals. This has expanded the testing volume and scope of tests with more and more immunoassays now becoming available on automated platforms. However there are certain challenges which need to be worked on. There is need to have more high throughput equipment. This saves space, manpower, and cost. More tests currently available only on ELISA need to be automated on one single platform. Issues like hook effect need to be worked out and systems to be created to nullify these errors. There is need to harmonize methods, biological references ranges amongst various manufacturers. Efforts also needed to have multianalyte calibrators as available for clinical chemistry. As technological innovations are moving at a rapid pace, I am hopeful that majority of these challenges will be resolved in coming years”.

Dr Barnali Das

Dr Barnali Das

Consultant, Laboratory Medicine, Kokilaben Dhirubhai Ambani Hospital

In the immunochemistry sector, the roadmap for laboratory medicine, involves strategies for harmonizing, communicating, and integrating with all stakeholders, like, clinicians, diagnosticians, and IVD industry, in order to formulate guidelines for assisting in correct measurement, diagnosis and management of diseases and reduce the cost burden, while maintaining quality. In this pandemic, processes need to be streamlined in laboratory medicine to ensure provision of reliable and timely test results, appropriate alliance with brain to brain loop, thus enhancing quality of care and patient safety.

The implementation of total cost of ownership (TCO) and Artificial Intelligence are instrumental in the transformation of the laboratory, more specifically, influencing clinical validation, procedure efficiency, data handling, productivity, and much more. AI helps in computing risk stratification score of laboratory data and clinical data using expert system and evidence based guidelines. It is important to manage the competing pressures of quality and cost for sustainability of any laboratory, and also introduce novel approaches for reducing costs without sacrificing quality.

Way forward

Immunochemistry analyzers are just now beginning to replace clinical chemistry and immunoassay as new or improved assays are being added to the test menus incrementally. Customer choices exceed combinations of needs in the immunochemistry market, which has more than 100 immunoassay analyzer models. Facing a high degree of competition, manufacturers modulate forecasts by shortening product cycles with new launches or adding value on existing installs.

There is heavy pressure for quality, error-free results to ensure patient satisfaction. This forces labs to lean toward high throughput and more automated systems with effective workflow solutions. Growing volumes due to an increase in the number of insured patients will encourage automation in laboratories. With a deficit in laboratory personnel, managing clinical laboratory flow is becoming difficult. Today’s scenario demands laboratories to seek the help of systems that have a high throughput, owing to growing volumes and also offer remote data acquisition capabilities. Implementing informatics is critical, and the automated analyzers built today offer a full suite for barcode readers, rack detection systems, and sample/plate identification modules to avoid plate or sample switch. Market participants of this highly competitive market are expected to continue infectious disease immunoassay product development and menu expansion.

Reagent sales typically comprise approximately 85 percent of fiscal revenues from any single system. Instrument placement is necessary for reagent sales. Therefore, many competitive factors in the immunoassay testing market lie with the instrumentation platform. The installed base of an instrument allows for an increase in test sales. When deciding on a particular testing platform, central laboratories value integrated and automated solutions. The number of tests offered for an instrument promotes the installed base and future reagent sales. A majority of testing platforms are closed systems in which the instrument does not facilitate tests of another provider. The competitive advantage in this market lies with companies that offer a broad testing menu on an integrated and automated system. Servicing the instruments installed in the laboratory is another significant part of the value proposition market participants should offer. Test performance is yet another competitive factor. However, it is becoming difficult for market participants to stand out on the basis of higher sensitivity or other testing characteristics.