MedTech

Innovation in handheld space disrupts the ultrasound landscape

As AI, ease of use, and reduced costs become the hallmarks of handheld ultrasound, these devices could become as essential and common as a stethoscope.

Ultrasound technology has not only become widespread but also indispensable in the healthcare industry today. It is now the preferred imaging modality of medical professionals worldwide, helping them examine organs and detect, as well as treat, both minor and life-threatening medical conditions.

The growing use of ultrasound can be partly attributed to the fact that the industry understands the dangers of exposing patients to other forms of imaging like X-rays. Of course, apart from the safety factor, other crucial aspects of ultrasound like its non-invasiveness, low cost, and ease-of-use have also played a large role in its ever-increasing significance in the medical field.

As the imaging modality continues to advance, ultrasound equipment is becoming increasingly smaller, more compact, mobile, and cost-effective. From the advent of large, unwieldy systems to compact and portable ultrasound machines, imaging technology has undergone a marked evolution. In recent years, pocket-sized handheld ultrasound machines have been introduced, too.

While handheld systems became a reality only a few years ago, they are here to stay. The market for these miniature devices looks promising, thanks to their small dimensions, ready accessibility, and convenience. Although this style of ultrasound machine cannot provide the full range of exams that larger ultrasound machines can, they are nonetheless a valuable diagnostic tool in emergency and point-of-care settings and private clinics.

Startups are shaking up the market

Currently, the demand for handheld ultrasound devices is on the rise owing to the shifting trend toward home healthcare and remote patient monitoring to reduce hospitalization cost. Handheld ultrasound systems have been on the market for nearly a decade and are now gaining preference due to numerous growth drivers, including portability and affordability, and solutions to previous obstacles, like insufficient image quality and lack of technological infrastructure and training. These handheld systems are improving patient access to ultrasound technology, especially in underserved markets where healthcare resources are limited. Serving these populations has always been a priority for healthcare providers, but ultrasound systems were mostly clunky and expensive until recent years when manufacturers began launching mobile systems.

Historically, handheld ultrasound equipment market growth has been hindered by poor image quality, technological infrastructure challenges, and lack of trained technicians. New handheld systems are designed with embedded technology, including semiconductor chips, and artificial intelligence (AI) programs, which significantly enhance image quality. Additionally, the supporting infrastructure, such as wireless networks, connectivity, and software, has caught up technologically to handheld systems and unleashed their full capabilities.

It is expected that by 2023, the global market for handheld ultrasound will exceed USD 400 million, with more and more primary care physicians integrating the device into their practice. As AI, ease of use, and reduced costs become the hallmarks of handheld ultrasound, these devices could become as essential and common as the stethoscope.

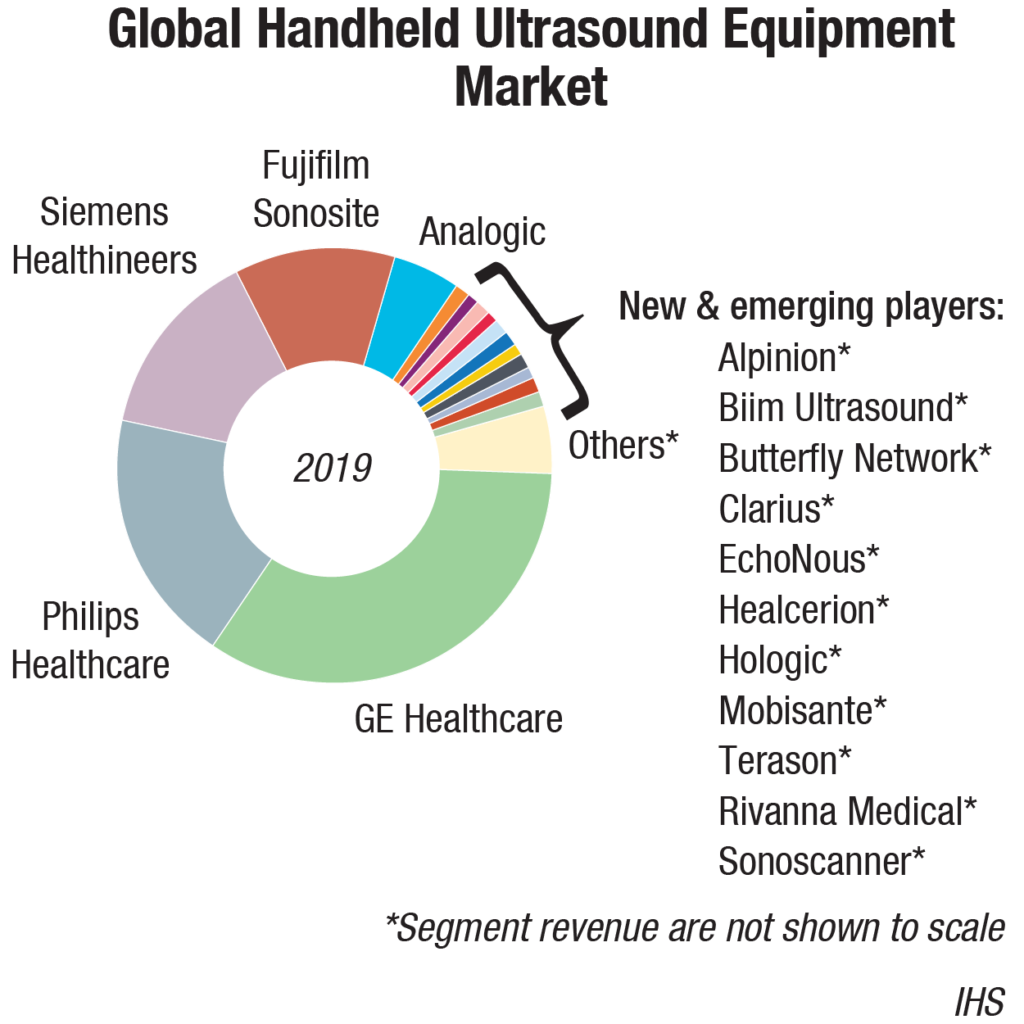

Major medical imaging manufacturers GE Healthcare, Philips Healthcare, Siemens Healthineers, and Fujifilm Sonosite account for the lion’s share of the global handheld ultrasound revenues. GE’s V-Scan was first released in 2010. This was followed by Mobisante, which was cleared by the US FDA in 2011. Philips also entered the field with its device called Lumify, which was cleared in 2015. While this large combined share may give the market the appearance of stability and control, in recent years, the handheld market has become a battleground between veteran imaging giants and ambitious tech startups.

From 2016 to 2019, a handful of startups entered the market and grabbed approximately 15 percent of the market share from the top companies. The strong sales networks and reputations of the major manufacturers are being challenged by innovative technology, low price points, and hype surrounding emerging players.

In August 2019, AI-enabled handheld ultrasound startup Exo landed USD 35 million in Series B funding. The startup is developing a portable ultrasound that is able to create a 3D image. The company is combining nano-materials, sensor technology and advanced signal processing, and computation to create the technology.

In September 2019, Butterfly has raised USD 250 million investment at a USD 1.25 billion valuation from the likes of The Bill and Melinda Gates Foundation, Fidelity, and Fosun Pharma, demonstrating their global intent. Its USD-2000 device is already on the market.

In November 2019, Portland-based startup Yor Labs raised USD 3.3 million to fund the development of a lightweight ultrasound system powered by AI. The stealthy startup was founded four years ago and plans to make ultrasound devices that are portable, handheld, and wireless.

Startups undercutting prices has left medical imaging giants reeling, but it is uncertain if this strategy is sustainable and scalable. Nonetheless, low prices have proven fruitful in the short term in generating publicity and increasing investor value for startups. The mission statements of the emerging players are fraught with ambitious statements about handheld ultrasound democratizing healthcare, replacing stethoscope, and living in every household, but these goals may be too good to be true. Are these nascent companies aiming for buyouts and licensing deals instead of working to establish themselves as standalone market players?

Market trends

The worldwide market for ultrasound equipment, expected to grow at a CAGR of 5.9 percent over the next 3 years, will reach USD 8.4 billion in 2023, from USD 7.5 billion in 2019, according to MarketsandMarkets. Factors like the increasing prevalence of target diseases; rising patient preference for minimally invasive procedures; technological advancements; increasing number of diagnostic centers and hospitals; and growing public and private investments, funding, and grants, are driving the growth of the global ultrasound market. However, stringent government regulations may restrict the growth of this market to a certain extent in the coming years.

The ultrasound market in developed regions like Western Europe, North America, and Japan is largely saturated and the outlook is for low- to mid-single-digit growth. While these markets will continue to account for the lion’s share of the world market, developing markets continue to represent a growth opportunity. In 2019, the fastest growth is forecast for Southeast Asia, Brazil, China, and India. That said, ultrasound market growth is slowing in many of the emerging markets, particularly China.

For several years, China has been the growth engine for the world ultrasound market, with consistently high double-digit annual growth. However, in more recent times, the world’s second-largest economy has entered a phase of slowdown and this is negatively impacting the ultrasound market. The annual growth rate dipped below 10 percent for the first time in 2019. With the Chinese OEMs capturing a growing share of the domestic market as they penetrate the high-end segment, China is becoming an increasingly tough market for the major multinational brands.

At present, the Mexican ultrasound equipment market is less high-end products, the overall price is located in the low-end. With the improvement of medical conditions and NAFTA implementation, more and more American manufacturing equipment will flow into the Mexican market. Ultrasound equipment from China is cheap, but because of the higher import tariffs on the local government, there is not much competitive advantage in Mexico.

Compared to the old generation of 2D ultrasound devices, 3D technology has added a dimension of depth, and 4D a dimension of depth and time. 3D and 4D ultrasound devices are becoming increasingly popular in Eastern Europe, especially in cardiology and obn ultrasound. The market for 3D and 4D is, however, not yet saturated there, mainly due to financial constraints. In other regions, such as Scandinavia, the reason for low market penetration of 3D/4D ultrasound is lack of acceptance among doctors. Research shows that doctors in Scandinavia do not consider 3D/4D ultrasound to provide more clinical value during diagnosis and are, therefore, quite reluctant. Convertors of images in older-generation ultrasound units were based on hardware, which was built in the ultrasound device. The new generation uses external computers, which perform the scan conversion. This has resulted in an increase of calculation power of ultrasound devices, and has led to major improvements in quality.

Technology trends

Technology trends

Despite the backdrop of global economic uncertainty, the ultrasound market is forecast to continue to grow relatively strongly in the coming years, with the following trends driving growth.

Increased AI integration will support better diagnostics. Artificial intelligence (AI) has had an impact on numerous aspects of healthcare delivery by enabling faster and more precise care. When it comes to handheld ultrasound, AI can reduce time-consuming and repetitive tasks and improve image quality, potentially leading to a faster and more accurate diagnosis.

Take, for example, an AI-powered cardiac application that guides clinicians to capture an image and then analyze it. This reduces the need for visual estimation and boosts diagnostic confidence as a result. It also helps create consistency across users, as one may be more liberal with his measurements, while another may be more conservative with hers.

AI will help enable primary care doctors scan, diagnose, and treat a wider range of patients across a broad spectrum of conditions, and provide crucial information more quickly. And the industry has only scratched the surface. As AI evolves, so will handheld ultrasound technology to bring in new users and enable new uses.

Handheld ultrasound devices will continue to be easier to use. Many doctors cite training and ease-of-use as barriers to adoption; however, this is slowly but surely changing. With increased technical advancements, handheld ultrasound devices are becoming more intuitive and easier to navigate.

There are also more readily accessible training opportunities, such as telemedicine capabilities, which allow technicians to share images and request insight from peers. This allows for remote supervision and addresses common training barriers like personnel shortages and unbalanced resource distribution.

On top of this, several medical schools have integrated handheld ultrasound training into their undergraduate and post-graduate medical curricula. In fact, in a recent study, medical residents found that by implementing pocket-size ultrasound examinations that took less than 11 minutes to the usual care, they were able to correct, verify, or add important diagnoses in more than one of three emergency medical admissions. As more current and future doctors learn how to use the device, they will better understand its benefits and will be more eager to integrate it into their practices.

Reduced market costs will drive increased adoption. Until recently, diagnostic imaging technology was not only clunky and difficult to transport, but also came at a steep price. Fortunately, innovation has reduced the size of handheld ultrasound devices, while bringing down costs. As a result, the market is at a tipping point and is moving from early adopters to mainstream users. Currently, there are more than 240,000 primary care physicians in the United States alone, and they continue to be seen as future adopters of handheld ultrasound.

Research update

Researchers at the University of California San Diego have developed an ultrasound-emitting device that brings lithium metal batteries or LMBs, one step closer to commercial viability. Although the research team focused on LMBs, the device can be used in any battery, regardless of chemistry.

The device that the researchers developed is an integral part of the battery and works by emitting ultrasound waves to create a circulating current in the electrolyte liquid found between the anode and cathode. This prevents the formation of lithium metal growths, called dendrites, during charging that leads to decreased performance and short circuits in LMBs.

The device is made from off-the-shelf smartphone components, which generate sound waves at extremely high frequencies – ranging from 100 million to 10 billion hertz. In phones, these devices are used mainly to filter the wireless cellular signal and identify and filter voice calls and data. Researchers used them instead to generate a flow within the battery’s electrolyte.

Currently, LMBs have not been considered a viable option to power everything from electric vehicles to electronics because their lifespan is too short. But these batteries also have twice the capacity of today’s best lithium ion batteries. For example, lithium metal-powered electric vehicles would have twice the range of lithium ion-powered vehicles, for the same battery weight.

Researchers showed that a lithium metal battery equipped with the device could be charged and discharged for 250 cycles and a lithium ion battery for more than 2000 cycles. The batteries were charged from zero to 100 percent in 10 minutes for each cycle.

Most battery research efforts focus on finding the perfect chemistry to develop batteries that last longer and charge faster. By contrast, the UC San Diego team sought to solve a fundamental issue – the fact that in traditional metal batteries, the electrolyte liquid between the cathode and anode is static. As a result, when the battery charges, the lithium ion in the electrolyte is depleted, making it more likely that lithium will deposit unevenly on the anode. This in turn causes the development of needle-like structures called dendrites that can grow unchecked from the anode toward the cathode, causing the battery to short circuit and even catch fire. Rapid charging speeds this phenomenon up.

By propagating ultrasound waves through the battery, the device causes the electrolyte to flow, replenishing the lithium in the electrolyte and making it more likely that the lithium will form uniform, dense deposits on the anode during charging.

The most difficult part of the process was designing the device, said An Huang, the paper’s first author and a PhD student in materials science at UC San Diego. The challenge was working at extremely small scales, understanding the physical phenomena involved, and finding an effective way to integrate the device inside the battery.

“Our next step will be to integrate this technology into commercial lithium ion batteries,” said Haodong Liu, the paper’s co-author and a nano-engineering postdoctoral researcher at the Jacobs School.

The technology has been licensed from UC San Diego by Matter Labs, a technology development firm based in Ventura, Calif. The license is not exclusive.

Outlook

Mutually beneficial deals are common in other technology markets. Buyouts and licensing agreements are a viable option for tech startups. It is an enormous task to grow from the ground up to directly challenge the Apples, Amazons, and Microsofts of the world.

Additional partnerships and acquisitions seem imminent, but whether a handheld startup has the master plan, cutting-edge technology, and gusto to take on the likes of GE and Philips is still to be seen. Nonetheless, the growing competition and innovation in the handheld space is undoubtedly shaking up the ultrasound landscape.

Second Opinion

Recent trends in ultrasound imaging

Recent trends in ultrasound imaging

Archana R

Associate Professor,

Osmania General Hospital

For the last four decades, ultrasound has been one of the primary diagnostic modalities with its unique advantages and limitations. These limitations, primarily limited field of view and user dependence, may be overcome by implementing truly three-dimensional (3D) imaging, automated image analysis, and post-processing tools.There has been a continuous advancement from A-mode to M-mode, B-mode, doppler imaging, contrast-enhanced ultrasound, US elastography, 3D and 4D Imaging, laparoscopic, intravascular, endoscopic, and intraoperative ultrasound.

Here we shall have a brief look at some of the recent and nascent innovations in ultrasound imaging. Other developments include harmonic imaging, pulse-inversion imaging, elastography, tissue characterization, portable ultrasound machines, deep learning, and artificial intelligence.

Super-resolution ultrasound imaging. Super-resolution ultrasound directly measures vessel density, inter-distance, size, unique flow pattern, and fractal factor. Super-resolution separates echoes coming from sources closer than the classic diffraction limit.

Ultrasound molecular imaging. Molecularly targeted contrast agents can visualize disease processes at the molecular level and monitor disease processes that are characterized by a differential expression of molecules on the vasculature like cancer or inflammatory diseases.

Radiomic ultrasound analysis. Radiomic describes the use of radiological data in a quantitative manner to establish correlations in between imaging biomarkers and clinical outcomes to improve disease diagnosis, treatment monitoring, and prediction of therapy responses.

High-intensity focused ultrasound (HIFU). HIFU can lead to local tissue heating, cavitation, and radiation forces, which can be used for a variety of therapies such as tissue ablation, image-guided drug delivery, sensitization to radiation therapy, immune stimulation, treatment of essential tremor, and immunotherapy in oncology.

Sonoporation. Microbubble-enhanced ultrasound is used to improve drug delivery to pathologic sites. Oscillating microbubbles promote vascular perfusion, vascular permeability, or tissue penetration. This process is called sonoporation and has been shown to improve the delivery of 100-nm liposomes to and into pancreatic tumors.

Digital beam forming. The beam former determines the shape of the beam. Digital transducers enable the ultrasound beam to be focused with greater precision and at higher frequencies, and can be used with broad-bandwidth transducers.

High-frequency imaging. High-frequency ultrasound imaging, using frequencies above 20 MHz, enable the imaging of superficial structures at very high resolution of 50 microns. Applications include the anterior chamber of the eye, intravascular ultrasound of arterial walls, skin, and cartilage.

Extended field-of-view imaging. It combines static B-mode with real-time imaging so that a large subject area can be viewed on a single static image. Extended field-of-view (FOV) images are obtained by sliding the probe over the area of interest and as the images are acquired, they are stitched together electronically, producing a single-slice image covering the whole area of interest.

Compound imaging. It combines electronic beam steering with conventional linear array technology to produce real-time images acquired from different view angles, and is useful for breast, peripheral blood vessels, and musculoskeletal applications.

Imagining trends with ultrasound

Imagining trends with ultrasound

Dr Jaya Nethagani

Prof. of Radiology,

MNJ Institute of Oncology & Regional Cancer Centre

Ultrasound (US) imaging uses high-frequency sound waves to characterize tissue. The transducer sends an ultrasound pulse into the tissue and then receives back echoes, which contain spatial and contrast information. Transcranial B-mode sonography is an easy-to-use bedside imaging modality to monitor significant changes of the brain parenchyma such as in malignant middle-cerebral infarction or intracerebral hemorrhage. The elevation of intracranial pressure can be followed with various neurosonographical techniques – measurement of the ventricular width, midline shift, arterial resistance, and optic-nerve sheath diameter. Thus, repeated imaging can be done without any harmful effects of non-ionizing radiation, and in a reduced time window. Monitoring of evolving hydrocephalus, using serial measurements of the third and lateral ventricles, can be used to guide therapeutic decisions such as the removal of a ventricular drainage. Other bedside uses include chest sonography in morbidly ill patients for pleural effusion, pneumothorax, consolidation, and eFAST in trauma.

Recent advances include fusion imaging where real-time US is usually fused with other imaging modalities such as CT, MR, and positron emission tomography (PET)/CT. 4D imaging, which is processing of multiple 3D images within a short period for a moving picture, is useful in fetal imaging and echocardiography. CEUS (contrast-enhanced ultrasound) involves administration of intravenous contrast agents containing microbubbles of gas, which is useful in focal liver lesions. Elastography will be useful in assessing tissue stiffness like in breast lesions and fibrotic livers. Tissue harmonic imaging provides high-quality images, which will be useful in improving pancreatic definition and differentiation of simple and complex cyst. Panoramic imaging has the ability to display an entire abnormality and show its relationship to adjacent structures on a single static image.

Research is being done to replace the piezoelectric crystals with tiny vibrating drums made of polymer resin, called poly CMUTs (polymer capacitive micro-machined ultrasound transducers), which are cheaper to manufacture. CEUS is expected to be used for children in the near future. Elastography is being researched for evaluating chronic pancreatitis, atheromatous plaque, venous thrombosis, graft rejection, and for cervical stiffness in pregnancy.