MB Stories

MRIs continue to see subdued demand…

…till COVID-19 is fully behind us.

The 2019-2020 coronavirus pandemic is anticipated to exert a massive impact on the healthcare systems across several countries worldwide. Some markets in healthcare are expected to witness a strong surge in demand due to their extensive utilization in combatting against these unprecedented times. At the same time, product areas that are affected by the postponement of certain medical procedures may witness a decline or reduced growth rate in 2021, since in a number of healthcare institutions these procedures continue to be on hold.

The MRI equipment is one of those product areas that are anticipated to witness a noticeable slow growth rate over the next couple of years. One of the major contributors are the advisory issued by key organizations such as the American College of Radiology (ACR), that magnetic resonance imaging equipment should not be used as an imaging technique for individuals with a COVID-19 diagnosis, or even those who are suspected of this infection.

This has further restricted the usage of this imaging modality, and since all the non-priority medical procedures have been put on a temporary hold, the reduced demand for this equipment further hurt the industry.

Key market players have anticipated major imaging modalities such as magnetic resonance imaging equipment to witness a decline in sales due to delay in installations, and the refocusing of the investment decisions.

Indian market

The Indian MRI equipment market for 2020 is estimated at ₹1307 crore, and 257 units, by volume. This is an 11 percent decline in volume and a 26 percent decline in value. This may be explained by a slight drop in the unit price of 3T and 1.5T systems, and an increase of the refurbished systems in the overall pie.

| Major vendors* in Indian MRI equipment market – 2020 | ||

|---|---|---|

| Tier I | Tier II | Others |

| Siemens, GE, and Philips | Toshiba and Hitachi | Esaote |

| *Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian MRI equipment market. | ||

| ADI Media Research | ||

The premium systems, 3T and 1.5T continue to dominate the market with a combined 85 percent share by value. These two segments each contribute about 42 percent by value, albeit by volume 1.5T sells almost twice than 3T systems. The refurbished machines in 2020 saw an increase over 2019, defying the trends of 2019 and 2018, when they had been stagnant, in spite of declining prices.

The segment continues to be dominated by Siemens, GE, and Philips. Toshiba and Hitachi are the other brands with some presence. This estimate includes 12 percent GST and third-party items, which amount to approximately 8 percent of the price of the equipment.

The decline in the market is attributed solely to the pandemic. It is expected that by end 2021 the sector will be back on track. As per the trend, the large hospitals and government, in spite of budgetary pressure are not expected to compromise on the quality and will continue to buy the high-end machines. It is the PPP medical facilities that make do with the low-end and refurbished models. By brand, Philips is quite successful with government hospitals, whereas GE’s focus is on the private sector.

Global market

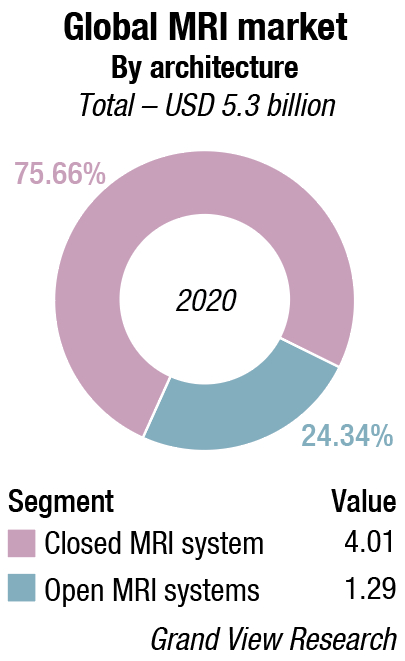

The global MRI market size was valued at USD 5.3 billion in 2020 and is expected to expand at a compound annual growth rate (CAGR) of 6 percent from 2021 to 2028. Advancements in diagnostic techniques like open MRI, visualization software, and superconducting magnets are fueling the growth of the MRI market. The recent advances seen in MRI technology are mainly on the software. These software advancements help in enabling faster contrast scans and simplifies imaging workflow.

The development of cardiac pacemaker compatible MRI systems is also expected to propel the market growth in cardiology segment. Furthermore, various paramagnetic contrast agents such as gadolinium-DTPA are used as an intravenous injection to provide sharp, precise, and accurate images within a shorter time frame.

MRI banned for COVID patients

COVID-19 has majorly impacted the outpatient imaging services. New York Metropolitan Health System reported 87 percent reduction in the outpatient imaging services, thereby, expected to impact the MRI market.

Various recent advancements such as diffusion and diffusion tensor imaging with tractography, neuroimaging including MR spectroscopy, perfusion imaging, and functional imaging using the bold technique are gaining popularity. Also, the growing development of intraoperative MRI and usage of the same in various applications such as neurosurgery are finding application. Diffusion-weighted MR imaging is mainly used to detect stroke within 30 minutes of its occurrence. Therefore, advancements in MRI machines to enhance its usage for various applications is expected to drive the market growth over the next 7 years.

High magnetic frequency MRI systems are gaining pace, and various universities are conducting research or studies on these systems. Scientists at the University of Minnesota performed an MRI of the human body using 10.5T MRI machine. This machine is expected to open new avenues in diagnosis of a wide range of diseases such as Alzheimer’s, heart disease, diabetes, and cancer.

Despite various advantages associated with MRI system, the costs incurred in buying and installing these machines is significant, which in turn is impacting the market growth especially in the developing regions. An average cost of a low to mid strength MRI machine is more than USD 1 million. In addition, increasing requirement of depleting deposits of helium gas for cooling of MRI machine is resulting in increasing wait time and is reducing productivity. Delayed product approval and frequent product recalls mainly due to stringent regulatory framework is also deterrant.

Architecture insights. The closed MRI system segment dominated the market and accounted for the largest market share of 75.8 percent in 2020. The closed MRI system uses powerful magnetic fields and high-frequency radio waves to obtain detailed images. Closed structure enables getting detailed slice selection and error free analysis.

Patients in the closed MRI may feel claustrophobic and disturbed due to its loud noise. These problems may result in inaccurate results. Some of the market players are focusing on developing wide bore and open MRI systems, which are suited for claustrophobic and oversized patients. Makers of pediatric MRI machines even add drawings and cartoons on MRI machines to calm children going inside the scanner. GE Healthcare’s Adventure series of MRI systems is specially designed for pediatric imaging.

However, closed MRI system is always preferred by the radiologists. Various clinical trials are also being conducted to check the efficiency of the open MRI systems for the diagnosis of diseases in neonates.

Field strength insights. The mid-field strength segment dominated the market and held the largest market share of 35.3 percent in 2020 and is expected to experience significant growth. These field strength MRI machines helps in capturing image with higher precision and are available in comparatively affordable prices. Low field strength MRI machines have field strength lesser than 1.5T, mid-field MRI machine have field strength ranging from1.5T up to 3T, and high field MRI machine has field strength more than 3T.

The low field strength MRI machine segment is expected to see a gradned exit. They are getting replaced by mid field and high field strength MRI machines mainly due to their image clarity and integration with AI.

Various research studies are being conducted to understand the efficiency of high field strength MRI machines in various clinical applications. Some players have already started developing high field MRI machines and are receiving approval from the regulatory body. Installation of these high field strength MRI machines in the universities is enhancing the study portfolio of the universities.

End-use insights. The hospital segment dominated the market and held the largest market share of 39.8 percent in 2020 mainly with the growing installation of MRI units in the hospitals. Increasing applications of rapid MRI (rMRI) in trauma and emergency care centers and rising number of MRI installments in teaching hospitals is expected to fuel segment growth.

The imaging centers segment is expected to experience a significant rise. Growing demand for non-invasive diagnosis is leading to the development of various individual centers which can provide services like MRI. Various medical professionals, who set up their owan centres, provide MRI at an affordable cost. .

The ambulatory care centers segment is expected to experience the fastest growth rate. Government initiatives to improve and increase the number of ambulatory care centers in rural areas is a priority.

Dr TBS Buxi

Head, Department of CT Scan and MRI

Sir Ganga Ram Hospital

MR technology has undergone substantial change. Efficiency is the key. The rapid acquisition technique by use of parallel techniques, which obtain images in shorter times, cover larger areas and of course using memory of previous data of same patients and using this finger printing technique for newer data helps in quick assessment and comparison. This is necessary in cancers, cardiac diseases, and other progressive disorders of liver and brain. Helium free scanners have reduced recurring expense. Artificial Intelligence is regularly being used, such as IR camera enabled for free breathing scans have replaced conventional breathing belt. Efficient powerful gradients have brought in better quality imaging. AI powered workflow and auto scan planning and superfast MR exams using Sense in 2D and 3D methods for all types of scans. Quantitative MR imaging in liver, head along with perfusion permeability APT, ASL in brain are more useful. MR RT planning is more precise and authentic for treatment purposes. Amide proton transfer imaging, arterial spin labelling in brain are proving to be useful. Iron deposition in the liver, heart, brain has been found useful in thalassemia. Cardiac imaging with volumetric analysis and valvular function and myocardial wall enhancement in acute myocardial infarctions are becoming popular.

Application insights. MRI systems used for brain and neurological imaging dominated the market and accounted for the largest market share of 24.2 percent in 2020 as scans produced are of superior quality than those by computerized tomography scans. Currently, 7T MRI machines are being studied only for brain and knee imaging due to the lack of advanced coils required for other clinical applications. Similarly, the breast imaging segment is expected to grow at a significant rate as the incidence of this cancer is gradually increasing, which has created the demand for identifying risk factors related to the disease. Therefore, MRI techniques help in providing quantitative information about cancer by identifying the biological and physical properties of tissue.

MRI is rapidly becoming the preferred method for spinal and musculoskeletal imaging. It uses the spin-echo technique to yield sharp contrast images between the spinal cord and subarachnoid space. This technique has wide applications in emergency and trauma care units. Spin-echo technique provides detailed analysis on internal injuries on soft tissues and spinal cord. As per the Association of Safe International Road Travel, around 20–50 million people are injured or disabled due to road accidents annually. MRI has wide applications in diagnosis of conditions such as osteoporosis, spinal infection, shingles, Scheuermann’s disease, spinal osteoarthritis, and spinal tumors. Early detection of these conditions is critical and decisive of treatment procedure and life expectancy.

Regional insights. North America dominated the market and accounted for the largest revenue share of 37.7 percent in 2020. Increasing incidence of chronic diseases in this region, which includes breast cancer, cardiovascular disorders, and neurological diseases is creating a demand for imaging analysis. The region is expected to maintain its dominance throughout the forecast period.

Technological innovations coupled with the growing incidence of chronic conditions are anticipated to spur the growth of the market.

Rapidly growing European countries such as the UK, France, and Germany that have a high per capita income and well-defined healthcare policies are showing increased demand for advanced diagnostic imaging modalities. In addition, constant technological advancement in the region along with large investment made in healthcare research, is expected to propel the segment growth.

Asia Pacific is expected to experience the fastest growth with the increasing geriatric population and growing demand for advanced imaging modalities. Moreover, the growing medical tourism industry in Asian countries is anticipated to augment the advanced medical imaging industry growth during the forecast period. Countries such as India, China, and Japan are creating growth opportunities with rapidly expanding healthcare service industry, presence of skilled healthcare staff, and advanced healthcare facilities and services at a lower cost than developed countries of North America and Europe.

The key players are developing MRI machines with high field strength to increase its adoption and usage in the field of medical imaging. Moreover, these players are forming strategic alliances to adopt and develop advance software which can increase the output of medical imaging.

For instance, in May 2020 the USFDA announced that the 510(k) clearance was granted to Synaptive Medical’s product offering of Evry. It is a point-of-care head MRI system developed for the provision of immediate access of diagnostic imaging for individuals requiring emergency care, especially for complications arising from COVID-19, and other neurological conditions such as ischemic stroke, neurological damage, or potential head trauma.

In February 2020, the Authority announced that the 510(k) clearance was granted to the world’s first ever bedside MRI, which is a product offering of Hyperfine Research, Inc.

Some of the prominent players include GE Healthcare, Hitachi Medical Systems, Siemens, Toshiba Corporation, Aurora Imaging Technologies, Philips Healthcare, Esaote, and Sanrad Medical Systems.

Global clinical research

At the recent virtual International Society for Magnetic Resonance in Medicine (ISMRM) 2020 meeting in August, Philips and University Medical Center (UMC) Utrecht, Netherlands, kicked off a research partnership to advance precision diagnosis through breakthrough quantitative MRI technology. The exclusive, multi-year research partnership will establish a global clinical research network with the aim of fully commercializing the technology, which has initially been developed at UMC Utrecht.

According to Philips, MR-STAT is a major shift in MRI, relying on a new, smart acquisition scheme and machine-assisted reconstruction. It delivers multiple quantitative MR parameters in a single fast scan, and represents a significant advance in MR tissue classification, fueling big data algorithms and AI-enabled integrated diagnostic solutions.

Dr Manoj Kumar

Sr Consultant, Radiologist

Manipal Hospital

Positron emission tomography–magnetic resonance imaging (PET–MRI) is a hybrid imaging technology that incorporates magnetic resonance imaging (MRI) soft tissue morphological imaging and positron emission tomography (PET) functional imaging.

Benefits in PET/MRI adoption

Imaging the most complex cases. PET/MRI can be used for advanced diagnostics in oncology, neurology and cardiology.

Saving time. Compared to separate PET and MRI examinations, the simultaneous procedure takes about 30 minutes instead of 60-90.

Improving registration. Due to the same patient position throughout the examination in simultaneous PET/MRI scanning, a health specialist will have a synergetic image with a better quality compared to separate PET and MRI.

Saving space. The 2-in-1 system helps to optimize room utilization within the healthcare organization, while providers definitely need two separate rooms for PET and MRI devices.

Applications

In general, applications for which PET/MRI is initially being used are those in which sequential PET and MRI are the standard of care. Applications capitalize on the inherent advantages of MRI versus CT, such as increased soft tissue contrast, use of hepatocyte specific contrast agents, and the ability to perform multi parametric evaluation including the quantification of radiotracer uptake combined with ADC values.

“At Philips, we are focused on supporting healthcare providers to realize first-time-right diagnosis through clinically relevant and intelligent diagnostics,” said Joland Rutgers, research and development leader for MR at Philips. “With this fast quantitative and single acquisition technology, enhanced with AI, MR-STAT will play a pivotal role in delivering the best diagnostic outcome at an affordable cost, benefitting both healthcare providers and their patients.”

Cardiac MRI becoming more widely available

MRI has been described for the past few decades as a futuristic imaging technology that will one day become the one-stop shop for cardiac evaluations. However, its expense, complexity, long imaging exam protocols, and long post-processing times have presented a barrier to wider adoption. That might be about to change with the help of new MR technologies released in the last few years, which experts say will change cardiac MRI’s fortunes and make it much more widely available.

Over the last 15 to 20 years, cardiac MR has been present, but has operated more in the research realm. But it is now coming into maturation and cardiac MR play a major role in the diagnosis of common cardiac conditions, such as cardiomyopathies, heart failure, and ischemic heart disease.

Some of the biggest obstacles to its adoption to date have been the complexity of the exam, the availability of expertise for people who really know how to run the exam and know how to read the exams, and also in the processing of the information.

There have been a lot of advances in MRI technology the past few years, with a concentration in new ways to speed up the image acquisition. This includes techniques like compressed sensing, parallel imaging, and echo sharing. In the past, a cardiac MRI exam would take about an hour to an hour and a half, but with current acceleration strategies one can now do a cardiac exam in probably about 30 minutes or less, and there are some papers out there saying it can be done in 15 minutes or less. So now it is much more comparable to echocardiography or other techniques that are faster and simpler to acquire.

Another barrier to wider use of cardiac MR is the time required to post-process images. But vendors have recently introduced new technologies to greatly speed up this process.

The analysis side has always been an area that is somewhat laborious for the practitioners because one needs to sit down and spend maybe another hour or so analyzing all the data. But now, with some of the new software platforms, especially more recently using AI, one now have a much more automated way of analyzing the images. And not just for more common parameters like ejection fraction, but also for tissue characterization to look for fibrosis. AI is playing a significant role in cardiac MRI automation to speed workflow and quantification. These technologies will become mainstream in the next few years.

AI is now incorporated into several MRI functions, including the third-party Arterys MRI post-processing software offered by several MRI and advanced visualization vendors. AI is also being incorporated into image reconstruction software being developed by vendors such as Philips, GE Healthcare, and Canon.

MRI has unique characteristics compared to CT and echocardiography. CT is pretty good at anatomical imaging to look at structures and coronary artery disease. MR on the other hand can also look at morphology, function, metabolism, and perfusion all in one imaging exam. MRI can look at the T1 and T2 mapping (which highlights either the water or fat in the body) and identify the content of the extra cellular spaces within the heart muscle. This can help identify fibrosis, which is a marker of disease in cardiomyopothies such as hypertrophic cardiomyopathy (HCM) and amyloidosis.

With this T2 mapping capability, MRI is now becoming the first-line imaging for diagnosing myocarditis for patients who are presenting to the emergency room.

Portable MRI may potentially disrupt medical imaging

Medical imaging has come a long way, having endured many trials and tribulations over time. Today, the practice of healthcare is incomplete without the intricate value provided by various imaging methods, including Computerized Tomography (CT) scans, Ultrasound, and Magnetic Resonance Imaging (MRI).

One disadvantage is that MRI scans often take longer to acquire than CT scans, and cannot be done in a portable manner, like portable X-rays.

However, a new venture may help reshape the way MRI is used and its future applications. Recently, Massachusetts General Hospital (MGH) announced the potential viability of a portable, low-field MRI device. W. Taylor Kimberly, chief of the division of Neurocritical Care at MGH, elaborates: “How can a portable low-field device that operates on a standard electrical plug change the paradigm? It can bring the MRI to the bedside, and it can do so in a hospital environment where there is metallic material nearby, and can do it safely because the magnetic field strength is lower.”

According to “In patients without COVID-19 (n = 30), neuroimaging findings were detected in 29 cases (97%). Twenty-nine patients (97%) also received conventional imaging (computed tomography, 6 patients; MRI, 23 patients). All POC [point-of-care] MRI findings were in agreement with available conventional radiology reports, except that 1 patient had a diffuse subarachnoid hemorrhage that was not observed on POC MRI(κ = 0.65; P < .001).” They also go on to provide findings in patients with COVID-19.

He concludes that “this experience demonstrates that low-field, portable MRI can be deployed successfully into intensive care settings. This approach may hold promise for portable assessment of neurological injury in other scenarios, including the emergency department, mobile stroke units, and resource-limited environments.”

Ultimately, only time and more evidence-based investigation will truly tell what the viability, accuracy, feasibility, and potential problems will be with the use of this new technology.

Moving ahead

Indeed, the world is moving toward more portable modalities of imaging. For example, in the last few years, the use of ultrasound technology has exponentially grown, with more companies offering portable solutions and promoting the use of point-of-care ultrasounds. Even formalized fellowship training programs are now available for physicians to gain more specialized clinical acumen and experience in these areas. This is also all in the context of AI technology, which is slowly gaining traction in the field of radiology.

However, just as with anything else that impacts patient care, clinicians, consumers, regulatory leaders, and the scientific community must maintain a high level of scrutiny to ensure that these new and emerging technologies have been thoroughly tested, supported, and proven, in order to ultimately maintain the highest standard of patient safety.