Industry

The COVID saga continues

The IVD market has been selectively propelled by the pandemic for most of this year, and the crisis is expected to continue well into H12021.

The COVID-19 pandemic has dramatically shaped the market, driving growth for some IVD tests while suppressing demand for others.

The 2020 market for IVD was substantial and growing, even before the COVID-19 pandemic hit.

IVD tests for cancer and infectious disease detection, transplant success, and pharmaceutical selection have added value to healthcare and improved clinical outcomes. Genetic tests for rare diseases and prenatal assessment are increasingly utilized. And now, the COVID-19 pandemic has highlighted how important an additional vitro testing is in a way that could not be imagined last year. Of the total IVD market, USD 9 billion is estimated to be COVID-19 testing, both molecular and antibody.

Prior to the COVID-19 pandemic, the IVD market was substantial and growing, and that portion of the market was estimated to reach USD 74.3 billion. Growth areas apart from COVID-19 include other infectious diseases (particularly respiratory pathogens), liquid biopsies, companion diagnostics, and critical care and hematology tests.

Some areas of in vitro testing have been negatively affected by the pandemic, however. These include noninfectious disease immunoassays, diabetes, and histology/cytology tests, which originate with doctor visits. Doctor visits have been impacted by social distancing and lockdowns during the year, though some catch-up visits and resulting tests are expected later in the year and in regions where COVID-19 has had less impact.

IVD tests based on polymerase chain reaction (PCR) make up a disproportionate share of revenue in the market this year, as PCR has proven to be the gold standard for COVID-19 detection. Where the most common type of nucleic acid test has represented approximately 10 percent of the market in past years, in 2020 it has surged to over 19 percent due to the technology’s favored use in COVID-19.

Financials from major IVD vendors in the second quarter of 2020 have produced mixed results reflective of this topsy-turvy market. Sales of COVID-19 tests are brisk, but other test areas were down in volume.

This affects different companies in different ways. Quidel, specializing in respiratory tests and point-of-care, announced that second-quarter revenue increased 86 percent and rapid immunoassay product revenue increased 270 percent.

Meanwhile, worldwide sales at Abbott Diagnostics took a hit despite the company bringing in about USD 615 million in revenues from COVID-19 diagnostic testing during the second quarter of 2020 (end-June 30). The company reported; sales dropped 8.2 percent to USD 7.3 billion in the second quarter of 2020.

Finally, Bio-Rad Laboratories also experienced a setback, reporting in its second quarter that the COVID-19 pandemic negatively impacted its revenue by 6.2 percent. How well these players perform in the full year will depend on their ability to capture test volumes from reopenings of offices and hospitals.

Molecular diagnostics will continue to drive growth in the IVD market, according to the Kalorama report. In 2019, there was still a degree to which vendors were persuading laboratories of the benefits of molecular approaches. In 2020, the challenge has been how fast systems can be set up and how much throughput they can offer as a war room-like mentality sets in at major IVD companies and the labs they service.

Real-time PCR systems have been highly utilized and supplies strained. Polls of labs even in July 2020 were still showing supply shortages.

New companies help to drive growth and 2020 is certainly no exception. There has also been a huge influx of product introductions from small, obscure companies. These have mostly targeted the low end of the price range and often had poor performance, while a small number of high-end automated systems are mostly limited to certain segments of the market, such as independent reference laboratories and centralized hospital laboratories.

Low-quality products from fly-by-night companies are the predictable result of shortages and the relatively basic resources needed to produce mediocre antibody test kits with a low level of quality control. However, leading companies as Abbott, Roche, Cepheid, DiaSorin, Hologic, Thermo Fisher Scientific, and Quidel currently account for the majority of the COVID-19 tests being performed in the US.

How long will this surge in revenue last? Kalorama analysts speculate that testing COVID-19 continues well into 2021, but it is too early to tell. A vaccine, or a global reduction in cases due to virus pass-through of the population, could theoretically reduce test IVD volumes, but it is not likely to eliminate the need for COVID-19 testing in its various forms.

The effect of the publicity that IVD has received as a result of the COVID-19 pandemic is difficult to measure but should pay dividends down the road, particularly with more serious preparation for new infectious disease threats. Machines designed for COVID-19, such as Abbott’s ID Now or Cepheid’s GeneXperts, may be removed from labs if the threat is perceived to have passed, but most likely systems will be converted to other purposes. This presages strong continued growth in testing and IVD test supplies.

The demand for IVD products is far broader in Asian countries

The IVD market is showing particularly strong growth in Asian countries with advanced healthcare systems. And that growth has been on steep trajectories since several years before the pandemic hit.

Polymerase chain reaction (PCR) tests, a mainstay in the IVD market, remain as the primary detection method for COVID-19. Efforts to curb the spread of the virus is driving rapid development of diagnostics, fast-tracking regulatory clearances and spurring producers to ramp up distribution. PCR systems are also used for diagnosis and screening of a wide array of other infectious diseases as well as testing cancer patients and for hereditary diseases.

In Asian countries where the number of elderly is rising very fast, where incomes are growing, personalized medicines are becoming more prominent, and new innovative techniques are growing in demand, the demand for IVD products is far broader.

Alongwith PCR systems, leading the growth are hematology analyzers. Together they account for about 45 percent of the region’s IVD analyzers and reagents market. In Japan alone, the diagnostic market estimates could reach USD 5 billion by 2026, including immunochemistry, molecular diagnostics, self-monitoring blood glucose meter, point-of-care testing (POCT), hematology, tissue diagnostics, hemostatic, and clinical microbiology.

In China, the IVD market is growing quickly as a result of a number of factors, including increased awareness of public health, an increase in the overall number of hospitals, more chronic Western diseases and an increased income in the middle class.

In Japan, the IVD market is growing due to an increase in chronic diseases that can be diagnosed and monitored more easily than in the past. Among the products showing the most growth are immunoassay and infectious disease IVDs, tumor markers, hematology, pathology, and genetic testing.

The South Korean market for IVD is projected to experience a CAGR of 5 percent until the end of 2025. IVD products used to diagnose infectious diseases account for the largest share, followed by oncology, which is the fastest growing segment owing to the increasing prevalence of cancer.

In Singapore, marked by an advanced healthcare system and high per capita spending, diagnostics has emerged as a way for earlier and better identification of diseases to control rising healthcare costs. Along with the country’s state-of-the-art infrastructure and high standards of medical practice, Singapore has become a natural choice for many global diagnostic companies to establish their regional business operations thanks to its strategic location and position as the most developed healthcare system in Southeast Asia.

Indian market dynamics – By segment

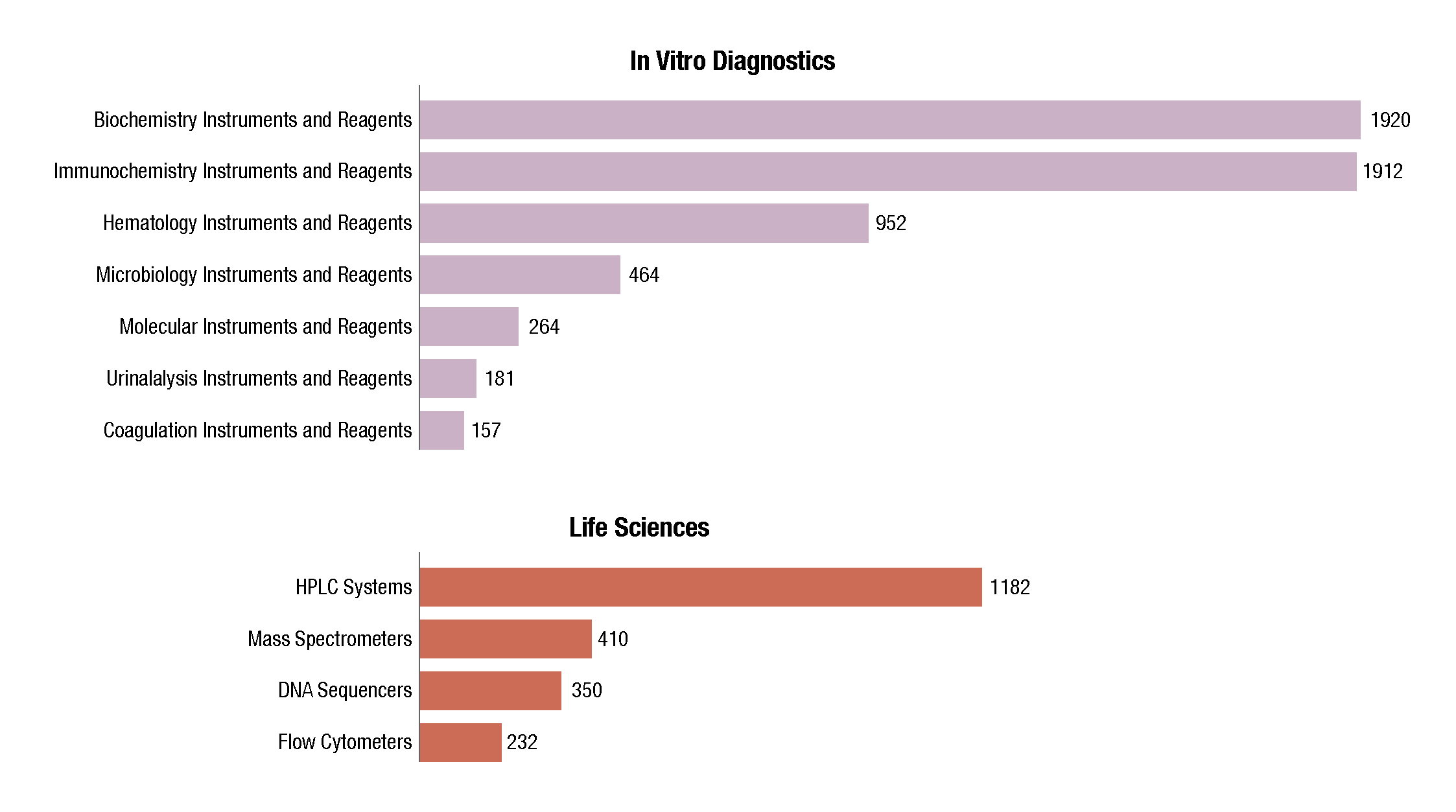

In 2019, the Indian biochemistry instruments and reagents market is estimated at ₹1920 crore, with reagents continuing to dominate at ₹1595 crore, at an 83 percent market share. The floor-standing analyzers are estimated at ₹93.41 crore and 670 units; benchtop analyzers at ₹92.44 crore and 1767 units; and semi-automated analyzers at ₹139.15 crore and 16,765 units. Almost 80 percent of floor instruments are on rentals; this figure is much smaller for bench-top. Semi-automated instruments are all procured, with almost none on rentals. The size of the market in 2019 has been calculated on assigning a monetary value to all the instruments installed, whether placed or sold.

The Indian immunochemistry instruments and reagents market, in 2019, is estimated at ₹1912 crore, with reagents dominating the market, with a 90 percent share at ₹1721 crore. The year 2019 saw an attempt by a handful of vendors for partial placement through their distributors, that is, placing the machine at a certain service revenue. How much success this model has and the extent it contributes to the bottom line will only be seen in the next couple of years. Competition continues to be cut-throat, margins are under pressure, and attempts are being made, not always with success at imposing penalties for not meeting commercial commitments of number of tests run by the laboratories to the vendors in a specific period.

The Indian HPLC market is estimated at ₹1182 crore, with 5500 units. The belly of the market continues to be the conventional, basic models with an 81 percent share by volume and 68 percent share by value in 2019. The vendors expect the market to increase at 7–8 percent per annum over the next three years, as compared to 12 percent earlier.

The Indian hematology instruments and reagents market in 2019 is estimated as ₹952 crore. Reagents constitute 60 percent of the market at ₹575 crore, and instruments, all fully automated, the balance at ₹377 crore. The hematology instruments market may be segmented as 3-part and 5-part analyzers. Within the 3-part analyzer segment, the single-chamber is a dying breed, and the laboratories are opting for its double-chamber counterpart, which contributes 86 percent to the total instruments market by volume. Within the 5-part analyzers, the entry-level or standalone analyzers are the preferred ones and are largely purchased. Within the high-level 5-part analyzer category, the basic model with an auto loader is more popular. However, the discerning customer opts for the high-end analyzer, with a throughput of 200–300 samples per hour that can create four to twelve slides from a single sample aspiration; and 140 slides can be prepared per hour. A handful of buyers also opt for a series of connected hematology work cells so that the lab can now streamline workflow with smart workload balancing and advanced analytics, providing relevant and thoughtful.

Indian diagnostics market

₹crore – 2019

workflow efficiency, while delivering comprehensive and accurate patient results. The 5-part high-level analyzers are almost all placements and are in a very few cases partially placed.

The Indian market for microbiology instruments and reagents in 2019 is estimated at ₹464 crore. The instruments-based reagents are estimated as ₹259 crore in 2019, a 55.8 percent share of the total market, non-instruments reagents at ₹155 crore, at a 33.4 percent share, each having increased by 10 percent over 2018. The balance contribution was made by instruments, the market size estimated at 540 instruments, valued at ₹50 crore, largely constituting of identification and antibiotic susceptibility analyzers and blood culture analyzers.

The Indian mass spectrometers market is estimated at ₹410 crore in 2019 with 260 units. 2019 saw major price erosion in this segment with poor credit facilities available and, thus, low allocation of funds for capital equipment. If this situation continues and pharma companies stay away from investing, downtime will be huge if this vacuum-based system goes down, as much advanced preparation is required and a proper solvent that does not contaminate the system is mandatory. In 2020 a 6-7 percent growth is expected. With the coronavirus outbreak some shortage of raw material is anticipated as the formulation industry has an estimated 3-month inventory.

The Indian market in 2019 for DNA sequencers is estimated at ₹350.5 crore. It may be segmented as capillary sequencers, NGS, and DNA-extraction kits. NGS continues to dominate the segment, with 69 percent share by instruments and 72 percent share by consumables, by value. The highest adoption is in the clinical market, which in 2019 saw an increase in demand of 25 percent, primarily from the large genomic testing labs and specialized labs. The genomics space in India is estimated as a ₹450 crore industry. Post-COVID lockdown, genome sequence information from the virus is helping researchers identify transmission patterns of the virus in minute detail. Scientists at NIBG, GBRC, CCMG, and IGIB, apart from other observations, are keeping track to whether the A2a or the O strain gain more steam in India. The field of genomics is getting a lot of traction from some large genome projects being undertaken by the government too. The Genome India project, spearheaded by the Centre for Brain Research at Indian Institute of Science aims to ultimately build a grid of the Indian reference genome to understand fully the type and nature of diseases and traits that comprise the diverse Indian population. The project is a collaboration of 20 institutions, including the Indian Institute of Science and selected IITs.

The Indian molecular diagnostics instruments and reagents market in 2019 is estimated as ₹264 crore.

Analyzers contributed ₹14 crore, and most were placed, on rentals. In the reagents segment, TB at ₹100 crore and HIV, HBV (hepatitis B virus), and HCV (hepatitis B virus) reagents estimated at ₹105 crore continue to have a combined contribution of 78 percent. India is on its way to eradicating tuberculosis by 2025. It is estimated that in 2019, the Indian market for oncology reagents was ₹12 crore, H1N1 reagents ₹6.5 crore, and reagents for other infectious diseases as HPV, CT/NG, STI, and dengue, that are also increasingly being diagnosed by molecular methods ₹26.5 crore.

The Indian flow cytometers market in 2019 is estimated at ₹232 crore. The market remained at the same level as 2018, by quantity, 110 units of analyzers and 21 units of cell sorters. Price points decreased marginally for analyzers, with about 20 percent installations on rentals. The cell sorters are offered in two categories, the high end and the basic models. Reagents, as expected, picked some pace and showed an upward trend by about 5 percent over 2018, which explains the slight growth in the total market despite a slight slack in instrumentation revenue.

The Indian market for urinalysis analyzers and reagents in 2019 is estimated at ₹181.75 crore. Reagents continue to dominate with an 80 percent share, valued at ₹145 crore. The fully automated analyzers segment is estimated at ₹16.75 crore, with integrated analyzers and urine chemistry instruments being almost similar in numbers. In the semi-automated instruments category, amounting to ₹20 crore, the entry level continues to hold sway by the number of instruments procured at 1680 units; albeit the high-throughput instruments bring better revenue, ₹720 crore in 2019.

The Indian coagulation instruments and reagents market in 2019 is estimated at ₹157 crore. While reagents are estimated at ₹144 crore, semi-automated instruments 750 units valued at ₹7.5 crore, the fully automated instruments at ₹5.52, crore is merely a value estimated on 60 units of placed instruments. Almost all the fully automated instruments are now on reagent rentals, including the government procurement. A couple of high-workload laboratories in government hospitals have gone one step further and negotiated CPRT (cost per reportable tests) terms. Many instruments are replacements, while others may be change in brand or for new set ups, including hospitals, primary healthcare centers, diagnostic centers, and research institutes.While the PT, aPTT, and TT tests continue to be the mainstay, this year the high-value D-dimer parameter testing, albeit constituting a small percentage, has been the saving grace in this segment. Blood banks are assessing the viability of fresh frozen plasma with the fibrinogen (Fbg) and factor VIII tests.

The Indian market for thermal cyclers, catering to the life sciences segment in 2019, is estimated at ₹117.6 crore. The traditional PCRs dominate the segment, by volume with a 69.65 percent share, and have a 31.55 percent share, by value. The real-time PCRs dominate the segment by value with a 49.32 percent share, and have a 28.86 percent share, by volume. The digital PCR, which was introduced in India around 2016, is the fastest-growing segment. Its share by value is 19.1 percent and by volume 1.49 percent. The traditional segment is gradually being eased out, in preference to the real-time PCRs, and some brands are offering a complimentary one with every real-time sold.

Outlook

The IVD market has been propelled by the COVID-19 pandemic for much of this year, and the global response to the crisis is expected to continue to drive diagnostics growth. Once the dust settles down, we can expect a few trends to come into play.

First, as diagnostics laboratories increasingly use fully automated instruments, they will decrease hands-on time, reduce batch testing, and provide doctors with quicker tests compared to non-automated instruments. Second, the integration of biomarkers and the availability of biomolecular tools are predicted to help in the development of a new set of condition-specific tests, thus creating new opportunities for the growth of IVD market size. And last, the IVD market will be driven by the use of personalized medicine products in treating cancer and other chronic diseases, along with increasing technological advances related to artificial intelligence and machine learning, which makes it possible to achieve higher levels of diagnostic precision.

One thing is certain. The current worldwide pandemic has clearly started to change the public’s and governmental view of the critical role that clinical laboratories play in public health and safety. It is now abundantly clear that without laboratory medicine appropriate public health measures and evidence-based care of hospitalized patients are simply not conceivable. Clinical laboratories have visibly demonstrated their vital role and value in the public health surveillance and patient care and management.