Industry

Tuck-in acquisitions poised to take off

A drop in M&A values and an abrupt halt to elective procedures have taken their toll on the MedTech industry in 2020. However, it is not all doom and gloom. The signing of two megadeals in August, unprecedented acceleration in digital health services, and a huge focus on fields like diagnostics suggest the industry is primed to bounce back in 2021.

Over the past 10 years, the MedTech industry has consistently performed well and experienced growth. With 2019 seeing the continuation of this trend, many predicted that further growth for MedTech would occur in 2020. Many companies across the industry were ending 2019 in a solid position, with some trading at 52-week highs and the industry overall growing revenue at over 6 percent.

The dearth of M&A observed in 2019 continued in the first 6 months of 2020 as COVID-19 disrupted all aspects of deal-making, from relationship building to the execution and closure of transactions. However, the economic hit from the pandemic and large drop-off in elective care threw that trajectory off course.

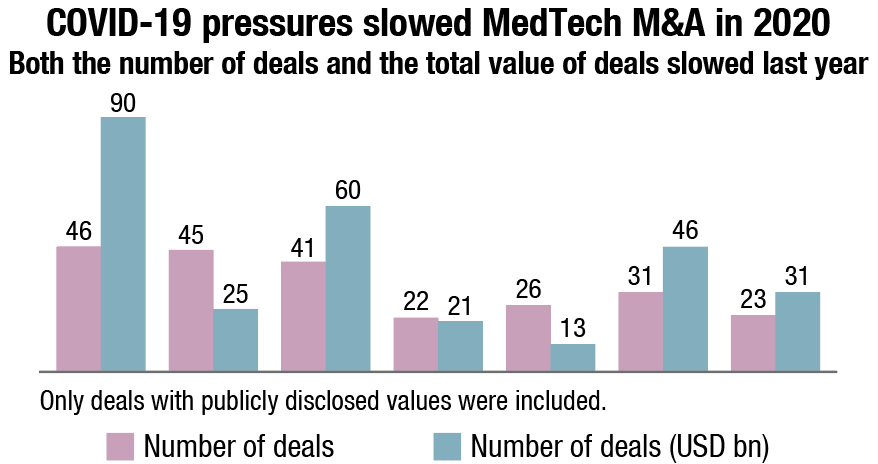

In 2020, the number of deals dropped from 31 in 2019 to 23, and the total value of deals dropped from USD 46 billion to USD 31 billion. The year was saved by a flurry of acquisitions in the third quarter after nearly no activity in the first half of 2020.

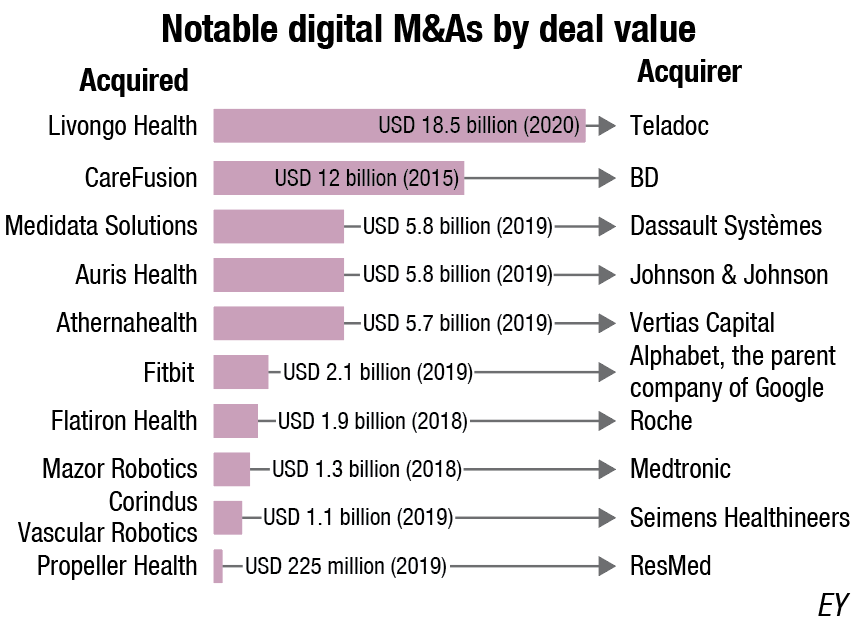

In 2020, MedTech deals were fewer in number but larger in size. The value of deals made during the first half of last year totaled about USD 2 billion, the value of deals made in the third quarter alone totaled USD 26 billion. Because telehealth is not typically considered part of the MedTech industry, the data does not include Teladoc’s USD 18.5 billion buy of remote patient monitoring company Livongo, which was one of the largest healthcare deals of 2020.

Perhaps the industry will look back on the first half of 2020 and see it as the calm before the storm. Indeed, if the uptick in deals announced in the second half of 2020 continues to be a trend, 2021 could finally be the year that MedTech unleash their collective deal making power. Two of the year’s largest life sciences deals showcase the potential. In August, Siemens Healthineers inked a USD 16.4 billion megadeal, acquiring Varian Medical Systems. In late September, Illumina announced it planned to spend USD 8 billion to acquire 100 percent of Grail.

Certainly, MedTech’s fundamentals suggest the time is right for M&A to take center stage. The industry’s firepower for deals expanded 41 percent in 2020 and is at an all-time high. During the year, the industry’s commercial leaders took advantage of the strong public markets to raise significant amounts of capital, primarily in the form of debt and follow-on offerings. At the same time, MedTech as a group only deployed 7 percent of their firepower through November 30, 2020. The result: major MedTechs have significant capital reserves to direct toward acquisitions in 2021 – if they choose to use it.

Where has MedTech been hit hardest?

Although general uncertainty and travel restrictions linked to the pandemic have affected all industries, the financial impact of COVID-19 on the MedTech industry has been primarily linked to the significant consequence of companies focusing on so-called elective procedures. The decline in elective procedures, hit the MedTech world in the fourth quarter. After rebounding in the second and third quarters from the sudden drop in March, April, and May, rising global cases of COVD-19 halted hospital operations at the end of last year.

The impact was particularly seen by MedTech with large hip and knee portfolios, such as Johnson & Johnson, Stryker, and Zimmer Biomet.

| Completion date | Acquirer | Target | Value (USD m) |

M&A focus |

|---|---|---|---|---|

| October 30 | Teladoc Health | Livongo | 18,500 | Diabetic care, healthcare IT, and patient monitoring |

| November 11 | Stryker | Wright Medical Group | 5400 | Orthopedics |

| October 2 | Invitae | Archer DX | 1400 | In vitro diagnostics |

| December 31 | Dentsply Sirona | Byte | 1040 | Dental |

| November 18 | Steris | Key Surgical | 850 | General hospital & healthcare supply |

| Evaluate Vantage | ||||

Stryker’s hips and knees business declined by 8.3 percent and 10.2 percent, respectively, and Zimmer reported declines of 1.3 percent for hips and 3.1 percent for knees. Meanwhile, Johnson & Johnson missed expectations for orthopedics by USD 92 million, with a miss of USD 12 million for hips and USD 38 million for knees.

Beyond orthopedics portfolios, Edwards Lifesciences saw a decline in transcatheter aortic valve replacement procedures in the quarter. Looking ahead to 2021, the company continues to anticipate underlying sales growth in the 15 to 20 percent range, with significant COVID-related challenges early in 2021 turning to a more normalized growth environment in the second half of the year.

Meanwhile, Boston Scientific reported losses across the company due to procedure declines. This represents a decline of (6.8) percent on a reported basis, (8.3) percent on an operational basis, and (8.0) percent on an organic basis, all compared to the prior year period.

While many executives for large MedTechs said the electives slowdown is expected to continue in the first months of 2021. Wall Street expects declines in elective care in the near term to continue as coronavirus cases keep rising. While the rollout of vaccines will likely help volumes, procedure comebacks are not expected until the second half of 2021, according to JP Morgan analysts.

At the top 35 MedTechs, growth gaps increased by USD 9 billion to USD 29 billion. With elective procedures resuming soon, companies seem to feel less pressure to preserve cash and more urgency to use their capital reserves for acquisitions. That attitude could shift as the COVID-19 cases surge in different geographies, however.

Opportunities are emerging for other fields

Opportunities are emerging in other MedTech fields. Look at diagnostics: in 2020, diagnostics companies have been at the forefront of combating the pandemic while also enabling care outside of traditional bricks-and-mortar channels.

The surge in coronavirus infections led to high demand for COVID-19 testing for diagnostics companies and laboratory networks in the fourth quarter.

Hologic’s molecular diagnostics revenue increased more than 450 percent, while Qiagen’s fourth quarter sales related to COVID-19 jumped almost 400 percent. Abbott reported a 110 percent increase in diagnostics sales compared to the prior year, driven by strong demand for its rapid antigen and PCR-based coronavirus tests.

Quest Diagnostics and LabCorp also benefited from strong demand for COVID-19 testing. LabCorp has reported 52 percent year-over-year revenue growth for the fourth quarter, and Quest reported a revenue increase of nearly 56 percent compared to the prior year.

Many industry analysts are expecting demand for COVID-19 testing to remain strong throughout the first half of 2021, and possibly longer, despite the rollout of vaccines and a nationwide drop in daily coronavirus cases. However, others see too much uncertainty to make 2021 forecasts and a possible decline in testing as early as the second quarter.

It will be interesting to see how the diagnostics segment develops as the furious pace of COVID-19 test development slows. 2021 could end up a bumper year.

Looking ahead to 2021

Across multiple industries, the pandemic has slowed growth and created new financial and operational pressures that were ultimately reflected in the year’s overall drop in life sciences M&A activity. Yet, while COVID-19 caused many acquirers to tap the brakes, it has simultaneously accelerated the broader transformation of healthcare.

The potential to use digital technologies and data analytics to deliver more convenient, affordable, and better healthcare has been trumpeted for years. But it took a global health crisis to demonstrate just how quickly healthcare delivery can move from its inconvenient, discontinuous, analog roots to a more convenient, seamless, digital experience. The rapid adoption of virtual care in the first half of 2020 is just one example of the health ecosystem’s evolution.

A report from EY predicts MedTech deal-making to jump in 2021 as companies are armed with a record high of roughly USD 500 billion in financial firepower. So far this year, the industry has seen a flurry of activity.

Hologic kicked the trend off in January with an acquisition of Somatex Medical for USD 64 million, and less than a week into 2021 added its second tuck-in with the acquisition of Biotheranostics for USD 230 million. PerkinElmer struck a deal to buy tuberculosis test provider Oxford Immunotec for USD 591 million and Thermo Fisher Scientific announced it will acquire privately-held molecular diagnostic maker Mesa Biotech for USD 450 million in cash.

The biggest deal over the first weeks of January was Steris’ purchase of Cantel Medical in a cash and stock acquisition of approximately USD 4.6 billion, followed by Boston Scientific’s announcement that it will purchase cardiac monitoring company Preventice Solutions in a USD 925 million deal and Philips’ plans to acquire Capsule Technologies for a cash consideration of USD 635 million.

While some companies will look for tuck-in acquisitions, a handful of deals over $1 billion could be expected.

Moving forward, there is no doubt that M&A will continue to be an important tool as diagnostics and MedTech reposition themselves for the future. As the specter of COVID-19 recedes, companies will need to disproportionately invest in data and capabilities that allow them to meet the demands of the ecosystem’s diverse and more demanding customers, especially payers and individual patients. Diagnostics and MedTech that delay investments in skills that enable more convenient and seamless care may find it difficult to compete with technology and consumer companies that see healthcare as prime segment for growth.