MedTech

Virtuosity in nuclear imagining

The future of nuclear medicine is bright, but significant challenges exist. Nuclear medicine represents a vibrant and viable specialty encompassing molecular imaging and molecular radiotherapy.

Nuclear medicine equipment thrives by continuous change. Twenty years ago, the introduction of PET/CT, followed by SPECT/CT and PET/MRI, fundamentally changed the field and required nuclear medicine physicians to learn the interpretation of multimodality studies.

Currently, the success of radioligand therapy and theranostics again tremendously affect the required knowledge, expertise, and, therefore, the training of nuclear medicine specialists. However, this is just the beginning. Digital PET, new PET tracers, a wave of new theranostic compounds, and the rise of artificial intelligence and machine learning will change the daily practice of nuclear medicine even more.

Radionuclide imaging assays diagnose, and phenotype disease provide prognostic information, survey the whole body for target expression, determine drug-target interactions, and assess treatment responses early after therapy initiation. More recently, 123I-iobenguane and 131I-iobenguane were approved for targeting the norepinephrine reuptake transporter in neuroblastoma and paraganglioma. Importantly, various approaches to targeting prostate-specific membrane antigen diagnostically and therapeutically have been deployed clinically in many countries. This list will certainly grow over the next 5–10 years. New advancements in technology and clinical research over the last couple of years appear poised to propel the specialty forward into new avenues of diagnostic and therapeutic capability.

Indian market

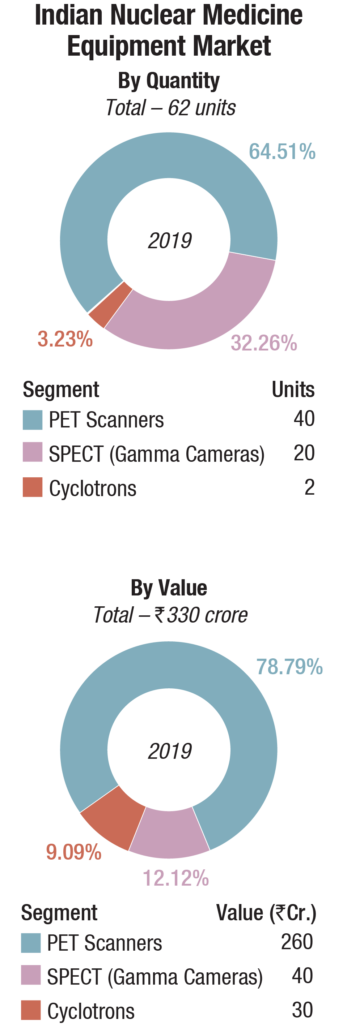

The Indian market for nuclear medicine equipment in 2019 is estimated at Rs 330 crore. The PET-CT scanners continue to dominate the segment, with a 64.5-percent share by volume, and a 78.8 percent share, by value.

Three digital PET-CT scanners were procured, one by HCG Bangalore, from Siemens and two from GE, one by Ruby Hall, Pune, and the other by Rajiv Gandhi Cancer Institute and Research Centre, New Delhi. These are priced in the Rs 20-crore range.

Biograph Vision-600 by Siemens is the first UDR detector with 3.2-mm LSO crystals and helps in visualizing smaller lesions. Biograph Vision is specifically designed to break through the limits of spatial and temporal resolution. With 3.2-mm crystals, it delivers high spatial resolution to reduce the impact of partial volume effect (PVE). Along with higher spatial resolution, a faster time of-flight also makes it easier to see small lesions. This helps quantify more accurately, and more confidently understand disease progression.

Dr BS Ajaikumar, chairman & CEO, HCG Enterprises Ltd., commented, “In cancer care, early diagnosis has proven to be the key, and treating it the right way the first time with proper staging results in achieving better outcomes. We at HCG are happy with digital PET CT, which transforms diagnosis and therapy to a much higher level. We are able to achieve precision and make disease staging even at the millimeter level and deliver appropriate treatment. This is the highest technology possible globally for image diagnosis. HCG has always invested in the best of technology and expertise for our patients for improved outcomes, testified by Harvard Business Review and the World Bank. This is another milestone for us in achieving our goals toward precision medicine and outcomes on par with global standards.”

Ruby Hall Clinic, Pune, has installed a digital PET-CT, Discovery MI by GE Healthcare. Discovery MI brings together the sensitivity of digital detection with the most innovative reconstruction technology available, the combination of time-of-flight and Q.Clear. In addition to advancements in reconstruction and detection technology, Discovery MI includes diagnostic CT innovations from the company’s Revolution EVO. It combines the Clarity Imaging System with the speed of the Performix 40 Plus tube with GE’s proprietary HiLight CT detector to deliver up to a 2x increase in spatial resolution. The innovative ASiR-V iterative reconstruction method comes standard to reduce CT dose by up to 82 percent at the same image quality in routine imaging across applications. And with Smart MAR, virtually eliminating streaks and shadows from metal artifacts, valuable time previously spent correcting images is saved.

The gamma camera with SPECT tomography and integrated CT scanner has a 32.2-percent share by volume and a 12.1-percent share, by value.

Two cyclotrons were sold, both by GE, value estimated at Rs 30 crore. IBA (Ion Beam Applications S.A.) is the other global leader for this product.

In India, GE dominates the segment and shares the space with Siemens. The refurbished machines also have a miniscule share. 2019 saw an entry of the PET-CT scanners in Tier-II and Tier-III cities, albeit with the basic models. 2020 has so far seen very low sales, and the market is expected to show a 15 to 20-percent drop over 2019.

Global market

Global market

The global nuclear medicine market size is expected to reach USD 12.6 billion by 2027, expanding at a CAGR of 9.5 percent, according to Grand View Research, Inc. Research and development of advanced technologies by the key players for diagnosis and treatment of diseases is expected to drive the radiopharmaceuticals market.

Rising incidence of cancer is one of the major factors expected to propel the market for nuclear medicine. Increasing prevalence of cardiovascular diseases is contributing to its growth too. According to WHO, cardiovascular diseases accounted for more than 17.9 million deaths worldwide every year. The number is expected to reach over 23.6 million by 2030.

Research and studies are conducted to enhance radiotherapy for various diseases like thyroid-related diseases, respiratory diseases, bone diseases, and neurological diseases. In July 2019, a research was published by a French investigator, demonstrating the use of hafnium oxide nanoparticle NBTXR3 as a radio enhancer to improve the response of radiotherapy for soft-tissue sarcoma. In addition, radiopharmaceuticals are being extensively used in molecular imaging, a technique involving molecules as biomarkers for specific molecular processes that determine the onset and/or progress of a disease. This is expected to drive the market for nuclear medicine during 2020–2027.

Government initiatives and funding for the development of new techniques are anticipated to drive the nuclear medicine market. In January 2019, European Fund for Regional Development (EFRO) and Kansen voor West Organization funded USD 7.67 million to NRG to FIELD-LAB for developing new nuclear medicines to treat cancer.

Also, presence of standard guidelines prepared by the regulatory authorities for radiopharmaceuticals is expected to accelerate market growth. In August 2019, USFDA published a guideline for non-clinical studies and product labeling that are not covered by USFDA and ICH guidelines for radiopharmaceuticals used in the treatment of cancer.

Product insights. Nuclear medicine is further segmented into diagnostic products and therapeutic products. Currently, single-photon emission computed tomography (SPECT) and PET techniques are widely employed in radiopharmaceutical diagnostic procedures. Factors like non-invasiveness, cost-effectivity, easy to handle, early diagnosis, and high sensitivity toward abnormalities in an organ function or structure, are driving the diagnostic nuclear medicine market.

SPECT dominated the global market for nuclear medicine in 2019 owing to its low cost and wide usage in different applications. Furthermore, digital SPECT scanners are being introduced in the market for nuclear medicine by key players to improve diagnosis.

PET is projected to be the fastest-growing segment over the next 7 years with the use of high-energy waves to produce 3D image, whole body scan for high accuracy, and ability to diagnose chronic diseases like Alzheimer’s disease, cancer, and respiratory diseases. PET uses radioisotopes for the diagnosis of the targeted organs. Adoption of PET as a diagnostic tool is rapidly increasing as it offers higher accuracy over other diagnostic techniques. Generally, to increase accuracy, it is integrated with X-ray and CT. Growing need for early and accurate diagnosis, along with the rising demand for better medical solutions, is fueling the radiopharmaceuticals market.

Medical cyclotron technology is considered to have revolutionized nuclear medicine owing to the clear evaluation of organs through molecular imaging. The global medical cyclotron market is poised to grow by USD 55.98 million during 2020-2024 at a CAGR of 6 percent, predicts Technavio. The growing need for the diagnosis and treatment of cancer and neurological diseases is driving the demand for medical imaging technology that uses radioisotopes. Medical isotopes are either made from nuclear reactors or cyclotrons. Cyclotrons can produce isotopes rich in protons and are thus, increasingly being used in radiation therapy and SPECT and PET imaging. Cyclotrons-produced radioisotopes help in obtaining highly specific activities through nuclear transformations. Such benefits of medical cyclotrons are expected to drive market growth in coming years. With the presence of several major players, the global medical cyclotron market is fragmented. Some of the major players include ALCEN, Ebco Industries Ltd., General Electric Co., Ion Beam Applications SA, Ionetix Corp., Siemens AG, Sumitomo Heavy Industries Ltd., TeamBest, and Varian Medical Systems Inc.

Indian Nuclear Medicine Equipment Market |

||

|---|---|---|

Major players* – 2019 |

||

| Tier I | Tier II | Others |

| GE | Siemens | Refurbished |

| *Vendors are placed in different tiers on the basis of their sales contribution to the overall revenues of the Indian nuclear medicine equipment market. | ||

| ADI Media Research | ||

The therapeutic segment includes alpha emitters, beta emitters, and brachytherapy. Beta emitters held the largest share of the market for nuclear medicine in 2019 owing to less damage to surrounding cells, and low energy levels. Furthermore, the most commonly used beta-emitting radioisotopes involve I-131, Y-90, SM-153, and Re-186. Brachytherapy is expected to witness the fastest growth over the forecast period. High accuracy and minimized risk of side effects are the factors attributed to the fastest growth of brachytherapy.

Application insights. Radiopharmaceuticals are used in the field of cardiology, oncology, thyroid, neurology, lymphoma, bone metastasis, endocrine tumor, and others. Cardiology is expected to be the fastest-growing segment with low cost of techniques and high adoption rate. Therefore, key players are focusing on development of new diagnostic techniques to combat cardiovascular diseases. However, the thyroid treatment segment is expected to show lucrative growth during the forecast period.

Regional insights. North America dominated the overall market in terms of revenue in 2019 owing to high investments in R&D, and support of the government toward use of medical isotopes are some factors driving the market. The Europe market also held a significant share in the global market in 2019.

The market in Asia-Pacific is expected to grow at a significant rate. Increasing geriatric population and awareness about nuclear medicine and molecular imaging are contributing to the growth of the radiopharmaceuticals market in this region. Furthermore, this region is focusing on development of radiopharmaceuticals for diagnosis and treatment of various diseases.

Market share insights. Key players in the global market for nuclear medicine includes Nordion, Inc., Eckert & Ziegler Group, GE Healthcare, and Bracco Imaging S.p.A., as well as government organizations like Department of Atomic Energy and Australian Nuclear Science and Technology Organization (ANSTO). These key players are implementing multiple strategies to maintain their significant share in the market. The strategies implemented include product development, business expansion, and collaborative development.

Technological insights. The current clinical standard for image reconstruction in PET is iterative algorithms, mainly ordered subset expectation maximization (OSEM). Recently developed systems commonly combine time-of-flight (TOF) capabilities and compensation for spatial variances in the scanner’s point spread function (PSF). While TOF mainly improves signal-to-noise ratio (SNR) at comparable convergence level and leaves standardized uptake values (SUV) comparably unaffected, PSF primarily increases reconstructed spatial resolution and has shown SUVmax increases by > 30 percent in clinical studies. Both TOF and PSF benefit the tradeoff between contrast recovery (CR) and SNR, but all conventional reconstruction methods share the principle limitation that adequate CR by increasing numbers of iterations/subsets will be at the cost of decreasing SNR.

Bayesian penalized likelihood reconstruction, like GE’s Q.Clear, has been introduced to offer full convergence of focal activity peaks and high SNR in homogenous areas within the same PET dataset. Q.Clear utilizes voxel-wise regulation of the iterative steps with a user-defined penalization factor β. Recently, using a GE Discovery IQ scanner with analog detectors, researchers showed an improved tradeoff between CR and SNR in a NEMA NU-2012 phantom protocol for Q.Clear with a β of 350 compared to PSF or OSEM (both without TOF).

Furthermore, the performance of TOF and PSF is dependent on the signal-to-background ratio (SBR) and lesion/sphere size. Previous studies that compared Q.Clear and conventional methods by only evaluating isolated reconstruction settings may therefore be of limited representativeness. However, a dedicated systematic evaluation of patient data is required for validation at different activity and acquisition protocols.

Opportunities

New opportunities in the diagnosis of and therapy for NETs, paraganglioma, pheochromocytoma, and bone metastatic disease – as well as, predictably in the near future, prostate cancer – are about to reshape nuclear medicine. Appropriate training will be critically important for integrating these approaches into the overall management of cancer patients.

New imaging biomarkers. The USFDA approved several imaging probes in recent years. These include the synthetic amino acid 18F-fluciclovine and the amino-alcohol 11C-choline for use in prostate cancer as well as Gallium-68 labeled DOTATOC to exploit the high level of somatostatin receptor expression of NETs. Several radiotracers targeting amyloid and tau are undergoing clinical evaluations and represent a key element in dementia research. PET imaging can interrogate the whole body for the expression of therapeutic targets. The presence and degree of target expression are associated with a therapy response. Thus, PET imaging probes have been introduced as predictive biomarkers. The degree of somatostatin receptor expression in patients with NETs, as measured with DOTATATE/TOC/NOC, permits predictions of peptide receptor radionuclide therapy responses. PSMA expression determined with PET stratifies patients toward PSMA-targeted molecular radiotherapy. Androgen receptor imaging provides prognostic information in patients with castration-resistant metastatic prostate cancer. The effects of antiandrogen drugs can be directly visualized using PET imaging of androgen receptor expression (pharmacodynamic biomarkers). Thus, PET biomarkers are now widely available for clinical and research uses. Nevertheless, they are still vastly underused, accounting for the small number of PET scans performed annually in the United States compared with the use of CT in oncology.

Treating and providing physicians as well as regulatory agencies and, at times, even health insurance companies increasingly recognize the value of imaging biomarkers. Deploying the large portfolio of PET probes and biomarkers rationally and effectively requires knowledge of biology, metabolism, drug-target interactions, cell surface receptor expression, and its association with the treatment response, and a solid background in medicine and associated clinical disciplines. A detailed description of the many radionuclide imaging biomarkers and approaches that are available for neurologic and cardiac applications is beyond the scope of this review. The growing number of imaging biomarkers strongly suggests the continuing growth of nuclear medicine and molecular imaging. Also evident is the fact that mastering the increasing diversity of diagnostic nuclear medicine and molecular imaging requires much more than four months of training.

Precision therapeutics. Precision or personalized medicine is often described nearly exclusively in the context of genomics. Underlying this concept is the notion that actionable cancer cell mutations may represent a cancer’s Achilles heel. Such actionable mutations include those of the epidermal growth factor receptor, BCR-ABL, BRAF, and many others. It was the success of imatinib for the treatment of chronic myelogenous leukemia and gastrointestinal stromal tumors that raised the hope that single oncogenic drivers could be identified and targeted successfully for most cancers. The goal of precision oncology has thus far remained largely elusive. Nuclear medicine techniques and assays usually are not discussed in the context of precision medicine, defined as the right treatment (drug or others), for the right patient, at the right dose, at the right time. Nevertheless, no discipline other than nuclear theranostics can provide noninvasive readouts of target expression and address the target structure successfully.

Nuclear theranostics. Several powerful nuclear theranostic approaches are already being clinically used, or are undergoing phase-3 clinical trial evaluations. The NETTER trial is an extremely convincing example of precision oncology. The expression of somatostatin receptors as a predictive biomarker was determined with 111In-DOTATATE imaging. Only patients with sufficient somatostatin receptor expression qualified for treatment with 177Lu-DOTATATE. Whole-body imaging, now done with 68Ga-DOTATATE, has a significant advantage over invasive tissue sampling, which is limited to few disease sites, and is subject to tumor heterogeneity and sampling errors. Somatostatin receptor-targeted PET molecular imaging and molecular radiotherapy are now approved by the USFDA and are reimbursed by the Centers for Medicare & Medicaid Services. The NETTER trial results unequivocally demonstrated highly significant benefits in progression-free and overall survival of patients undergoing 177Lu-DOTATATE versus standard-of-care treatment. This outcome was met with a great business interest, and Novartis acquired Advanced Accelerator Applications, the licensee of Lutathera, for USD 3.9 billion in the fall of 2017. Since then, Novartis has expanded its nuclear theranostic portfolio to include PSMA-targeted diagnostics and therapeutics.

On the basis of a phase-2 multicenter trial, 131I-iobenguane, a guanethidine derivative that is a substrate for norepinephrine reuptake transporters, was approved by the USFDA for the therapy of pheochromocytoma and paraganglioma.

In the United States, large-scale phase-3 trials, testing the diagnostic performance of various PSMA ligands labeled with 18F or 68Ga, are approaching completion or have been published. It appears quite likely that diagnostic compounds will gain USFDA approval before PSMA-targeted therapeutic compounds are reviewed and evaluated if the phase-3 clinical trials provide the anticipated results.

Other equally exciting nuclear theranostic approaches are emerging. The experts have identified the fibroblast activation protein as a tumor stroma target, and have developed a series of quinolone-based fibroblast activation protein ligands. 68Ga-labaled ligands accumulate with high specificity in target structures. Importantly, extensive stroma components have been observed across many cancers, suggesting that a theranostic radionuclide pair for targeting various cancers could emerge.

Challenges

Interpretations of PET/CT studies can require as long as one hour if the process includes obtaining patient history, which is often complex, and conducting careful comparisons with prior anatomic and molecular imaging studies. Given these complexities reimbursement rates for 18F-FDG PET imaging studies are low. Although AI and deep learning may aid in and expedite image interpretation and reporting in the future, these fields are still immature.

Financial viability. The lack of economic pressures in not-for-profit healthcare systems accounts, in part, for thriving nuclear medicine departments. In other words, the fiscal viability of nuclear medicine is less relevant in the European or Australian systems (mostly not-for-profit) than it is in the United States (for-profit) healthcare model. In public healthcare systems, the net profit is less relevant than the net benefit for patients. The independence of clinical departments is thus a matter of medical impact rather than financial profitability.

However, nuclear theranostics not only provides great opportunities for patients and thus for the physicians taking care of these patients, but also has the potential to change the nuclear medicine business model.

Training and licensing. Considering the increasingly broad scope of nuclear medicine, molecular imaging, and molecular radiotherapy, the need for much improved training and education is evident. Standardization is needed. Nuclear Regulatory Commission authorized user accreditation for radiologists and radiation oncologists after only 4 months of training, which defies logic. The molecular characterization of diseases is becoming increasingly complex, requiring a special and different skill set. PET/CT or SPECT/CT studies can be interpreted jointly with radiology. However, interpreting these studies jointly does not rule out the independence – in content and administratively – of the two specialties, which have substantial overlap but are inherently different. Nuclear medicine has deep roots in biology, biochemistry, metabolism, and medicine. Radiology is largely anchored in anatomy. Molecular radiotherapy and nuclear theranostics necessitate a thorough understanding of disease entities and molecular targets, sequence of therapies, radiation biology, radiation physics, instrumentation, internal dosimetry, management of oncologic patients and treatment side effects, and radiation safety, among other aspects.

The emergence of new radionuclide therapies has created an urgent need to reevaluate nuclear medicine training programs. The International Atomic Energy Agency recommends four years of dedicated nuclear medicine training (after 1–2 year of internship). This model has been applied in various places in Europe and Australia, where 4- to 5-year programs have been highly successful.

A 4-year training program that matches the educational standards applied worldwide should be implemented. Board certification and licensing should be contingent on meeting these standards and requirements. The first three years of the training program should be mandatory for any physician seeking dual board certification in nuclear medicine (e.g., radiologists, radiation oncologists, cardiologists, or internists). Whatever training model and certification process are adopted, the nuclear medicine community needs to approach these discussions with confidence, competence, and optimism. The diagnostic and therapeutic services developed in nuclear medicine will persist, but without adaptation and change, they will be delivered by others.

Way forward

The future of nuclear medicine is bright, but significant challenges exist. Nuclear medicine represents a vibrant and viable specialty encompassing molecular imaging and molecular radiotherapy. Nuclear theranostics is the most convincing example of precision medicine, as whole-body target expression that provides information for optimizing treatment approaches can be measured noninvasively. Completely revised board certification and licensing standards are needed to achieve optimized and integrated patient care.

Second Opinion

Dr Karuna Luthra

Dr Karuna Luthra

Consultant Nuclear Physician,

Department of Nuclear Medicine & PET-CT,

Jaslok Hospital & Research Centre

Nuclear medicine – Opportunities and changes in COVID-19 times

Today, COVID-19 compels us to change our mindset about health as well as business. This is an opportunity to correct, modify, and improve our approach and priority to healthcare. My wish list at this point of time for nuclear medicine includes the following:

Indigenous PET-CT scanners. PET-CT is the whole-body fusion-imaging modality, where PET, i.e., molecular functional images are superimposed on CT scan images. It is the imaging of choice for tumours, as well as medical conditions like PUO as also for some chronic inflammatory, neurological, and cardiac conditions. However, lack of availability and cost limit the widespread usage of this extremely powerful modality. Some promising steps for Make in India of PET-CT machines have been made, and now with the call for Atmanirbharta, I hope rapid indigenization of PET-CT systems will allow this modality to reach each and every teaching hospital, every medium- and large-sized hospital in our country.

Interventional nuclear medicine systems. Diagnostic yield as well as accuracy of biopsies is higher when they are taken from the most metabolically active site – something that can be assessed on PET-CT rather than blind biopsy or even USG/CT-guided biopsy. Similarly, ablative therapies like radio and cryoablation may be better when they are PET-CT guided. Robotic biopsy equipment is being used now for PET-guided interventions, and this is definitely on my radar. If these are manufactured locally and are made available at reasonable cost, this technology could be well utilized by every PET-CT department.

Software advancements. What used to be an option has now become a necessity – having remote access to nuclear medicine images and tele-reporting is required in times of social distancing, and rotational work patterns. Vendor software that comes with the machine with secure internet-based variable location access, improved PACS systems with fusion-image viewing capabilities, development and availability of better, interactive online PET-CT viewing software is the need of the hour.

Public-private partnerships. With the avenue of public-private partnerships in nuclear sector being opened recently, it is hoped that more medical isotope facilities for development of Indian version of Gallium-68 generators, newer F-18-labelled compounds, Alpha therapy radio-isotopes like Ac225, amongst others, will allow widespread and cost-effective imaging and treatment (theranostic) options for many needy patients.

Dr Parul Mohan

Dr Parul Mohan

Senior Consultant & Incharge Nuclear Medicine,

Mahajan Imaging & Fortis Hospital

PET-CT – Current status in India

PET-CT (positron emission tomography and computed tomography) is a nuclear medicine technique combined with computed tomography. Rising prevalence of various chronic diseases is leading to higher demand for more accurate scanning. At present, a combined PET-CT scanning is used to provide images that pinpoint the anatomic location of abnormal metabolic activity within the body. The combined scans offer more accurate and detailed diagnosis compared to the two scans performed separately. A rapidly aging population, and several diseases associated with aging, is another factor which facilitates market growth. The change in lifestyle along with aging is responsible for a number of heart issues. Hence, an early and accurate diagnosis is helpful. Moreover, developments of cost-efficient manufacturers in the upcoming years will propel future PET-CT scanner device market growth. Additionally, rising investments as well as increasing awareness are expected to motivate the market in the coming years.

In India, since December 2004, there has been a steady increase in the number of imaging systems. From stand-alone PET/CT systems with onsite cyclotrons, mostly in the government sector, today majority of the PET/CT scanners and cyclotrons are in the private setup. Scanners situated in different locations share the isotopes produced by one cyclotron. Increased awareness in people toward early diagnosis for various health diseases as well as affordability to these high-cost devices is a major factor for this growth. Rise in geriatric population in our country and increasing prevalence of diseases are expected to drive the market growth. Moreover, population is supposed to get more awareness about the PET-CT scanning techniques to diagnose several diseases. This would drive the market growth in India. The trend of investing in nuclear medicine is increasing and the current status of PET/CT in India is healthy and promising.

Dr Ankur Pruthi

Dr Ankur Pruthi

Consultant and Head, Department of Nuclear Medicine & PET CT,

Manipal Hospital

Nuclear medicine – What the future holds amid COVID-19 pandemic

Coronavirus infection (COVID-19) has reached a pandemic stage, spread across all the continents. We are pushed into unprecedented and unpredictable times when millions of lives have been affected. The infection has caused lakhs of deaths worldwide, and is having social and economic fallout. The world of medicine has been affected worst. Hospitals have seen a dip in patient numbers, admissions, and surgeries. The revenues have fallen and hospitals have constrained budgets for the times to come. Nuclear medicine specialty has also been severely affected owing to:

- Disruption in supplies of radioactive materials and radiopharmaceuticals

- Short-term expiry of most radioactive products

- Lock-down affecting patient and staff movement

The coming year presents multiple challenges for the nuclear medicine specialty. With every challenge, comes a hidden opportunity. I would like to highlight a few:

- Supply of radio-active medicines. We are currently importing prepared radiopharmaceuticals, non-radioactive raw materials, cold kits, etc., from multiple countries. Local production of these radio-pharmaceuticals is still at a nascent stage, despite a big indigenous market. Managing regular supplies will be an enormous challenge for producers, importers, and distributors owing to disruption in production and transportation.

- Need for self-reliance. There is increasing need for self-reliance for these products to tide over uncertainties. Local manufacturing may get a boost with increasing investments and public-private partnership (PPP) model. There is a huge demand for local production of high-quality radionuclide generators, Iodine-131, Lutetium, Yttrium therapies, and high-quality cold kits.

- Increased COVID-19 testing. COVID-19 testing will become a norm in hospitals before procedures and surgeries. In near future, we see increased availability of rapid kits for COVID-19 testing before routine procedures like PET CT.

- Remote-access for social distancing. Software will be sought for managing patient appointments, sending messages, remote reporting of scans, remote access to scanner consoles, PACS, HIS, etc. Alarms for social distancing may be a norm in the near future.

- Specific requirements. There will be an increased requirement of N95 masks, personal protective equipment (PPE) kits, hand sanitizers, gloves, etc. Robotic devices, which could provide technologists and nurses access to patients from a distance will be in demand. Also, there will be increasing demand for techniques for rapid disinfection of PET CT and SPECT CT scanner gantries, rooms, and other patient areas in the department.

- Preparing for future. Local production of medical equipment should be the core focus of programs like Make in India, considering a large market for such products. Currently, all major players have production units of CT, PET CT, SPECT CT scanners, and their components outside India.

I would end by saying that there is a huge challenge ahead. I hope that human race will succeed with strength and compassion.