MB's Take

Digital health – Weathering the cash crunch

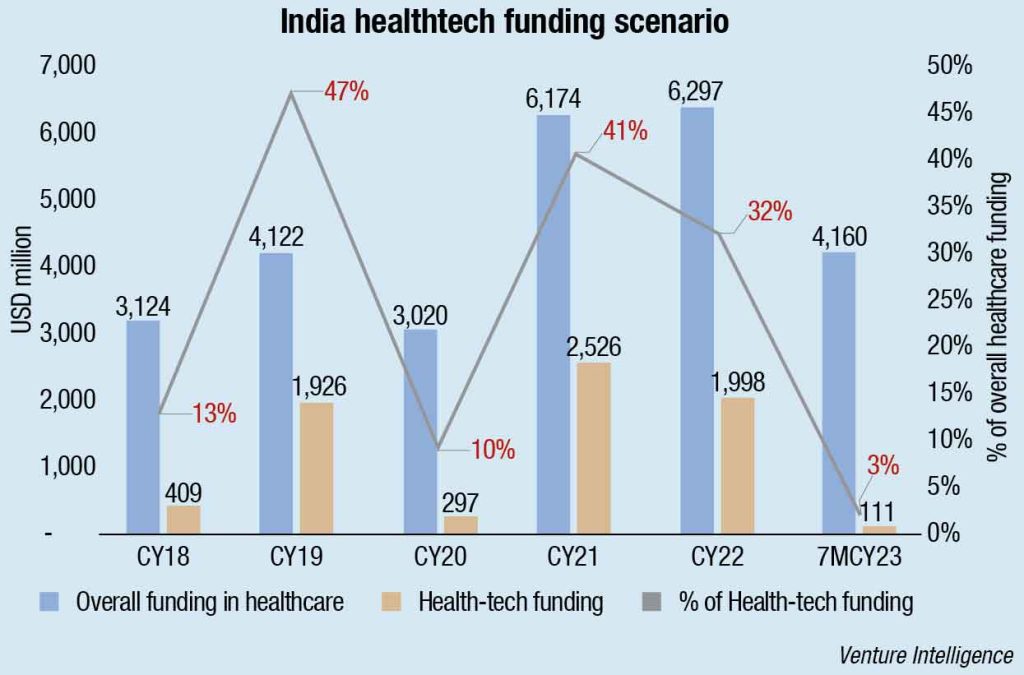

India’s USD 6.5 billion digital health sector is today at a challenging crossroad with private capital funding shrinking by more than 95 percent compared to two years ago. During 2023, the segment has received a meagre USD 111 million private funding in contrast to the record USD 2.5 billion capital raised in 2021. Adding to the funding challenge has been the tirade of negative news-flow that has gripped the sector over the past few months. For example, the largest player, PharmEasy’s ~80 percent valuation drop and corporate governance issues coming to light in the smaller names. Investor sentiment in this segment is clearly at the lowest in the last five years. In our view, the sector presently stands at the threshold of critical introspection which will need to be addressed before we can see the next leg of growth among the survivors. Over the next 12-18 months, companies will need to address five issues at hand before we can see the next wave of significant interest across the sector.

- The sector probably has less than 9 months of cash runaway left based on our analysis of the cash in hand of 120 companies in the segment; moving toward profitable growth will be a key factor to regain investor interest.

- While several companies in the space have started working on profitability, it remains to be seen how much impact the funding crunch will have on growth in the coming months.

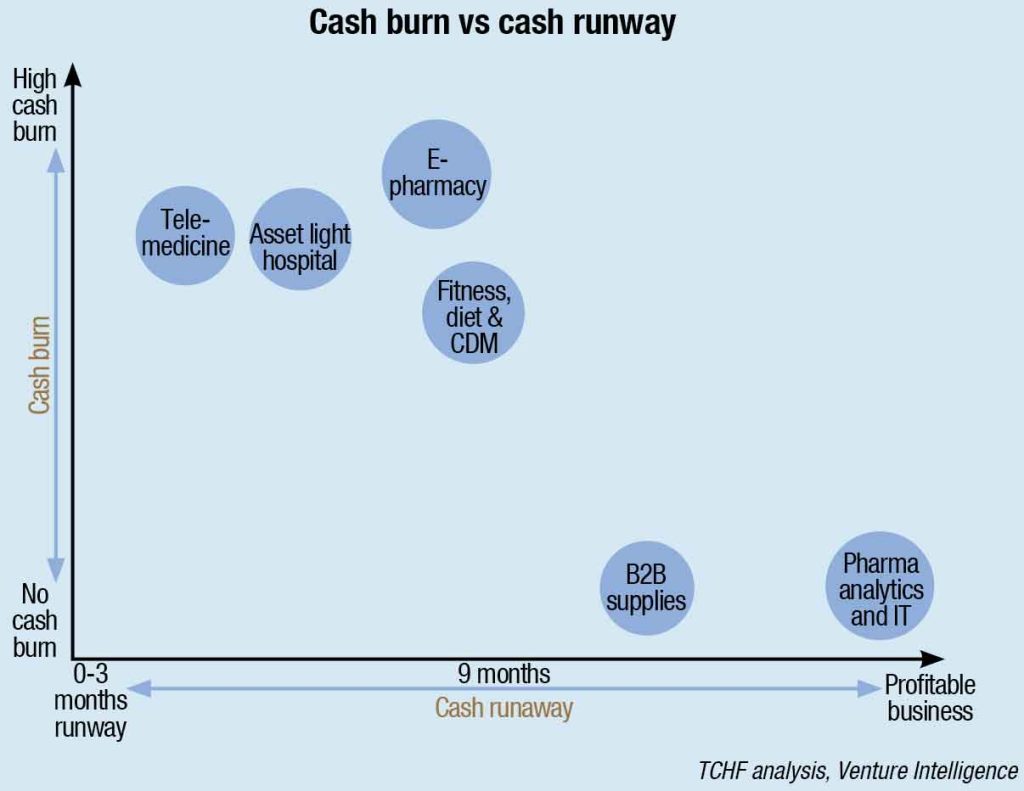

- E-pharmacy, the largest healthtech segment which attracted the lion’s share of funding in the last five years continues to remain elusive on its path to sustainable profitability. However, given the corporate backing of most players in this segment the cash burn and runway for this segment is less under question compared to growth challenges.

- Many standalone healthtech businesses like telemedicine and asset light hospitals are ceasing to exist as stand-alone business models given lack of scale; on the other hand, the B2B hospital supplies businesses face modest growth and marginal profitability; pharma analytics segment continues to remain a silver lining in the space.

- Finally, the triple burden of cash crunch, slowing growth concerns and elusive path to profitability are yet to reflect in valuation reset (baring a few like PharmEasy); the next 12-18 months will likely set a path in that direction.

E-health (E-pharmacy & E-diagnostics)

Profitability not in sight, omnichannel is becoming the way ahead

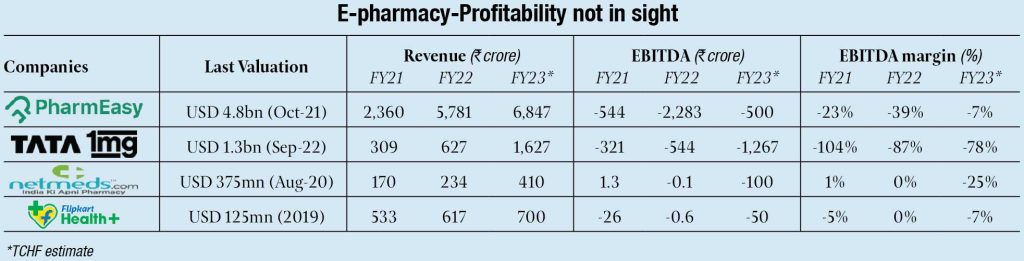

- The E-pharmacy segment has attracted ~USD 2 billion funding in the past 5 years and presently have about 9 months of cash run-way.

- The largest player PharmEasy has over the past year struggled with a failed IPO process thereby facing about 90 percent valuation correction. On the other hand, corporate backed platforms like Tata 1mg and Netmeds remain on a growth push (1mg grew ~160 percent in FY23 and Netmeds grew ~75 percent); however losses continue to be high. This segment has now taken an omnichannel approach (Netmeds plans to open 2,000 offline pharmacy stores in 12 months) funded by the parent balance sheet.

- Overall, this segment is expected to continue to see losses as they push for growth given the customer acquisition costs continue to remain high and stickiness is low. However, given the corporate backing of most players in this segment the cash burn and runway for this segment is less under question compared to growth challenges.

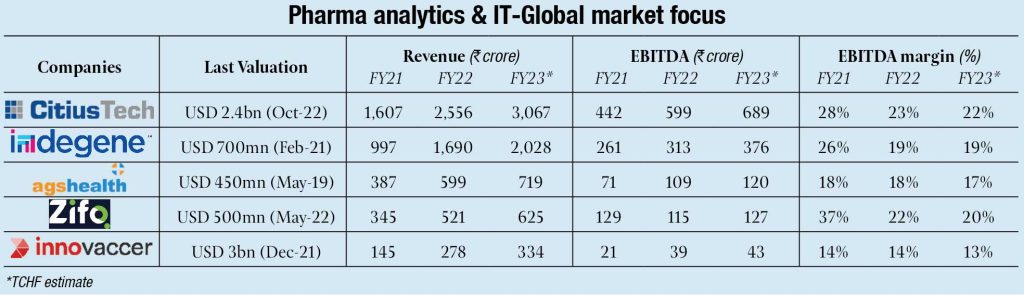

Pharma Analytics & IT

Global market focus: Enjoying high profit margins

- The Pharma Analytics segment has received USD 2.8 billion funding in the last few years primarily toward healthcare IT companies like Citius, Zifo and new age SaaS companies like THB, Innovaccer, Healthplix.

- The healthcare IT companies are highly profitable with stable EBITDA margins (~18%-25%). With several buyout funds (Bain, Carlyle etc) taking controlling stakes in these companies, it is likely to result in potential IPOs in this space (eg Indigene has filed its DRHP). Meanwhile, the new age healthcare software companies are loss making but have begun to show signs of profitability with the early mover in the space, Innovaccer becoming profitable.

- This segment does not have any notable financial stress and has a potential to grow ~15 percent+ with focus on scale being achieved through global markets.

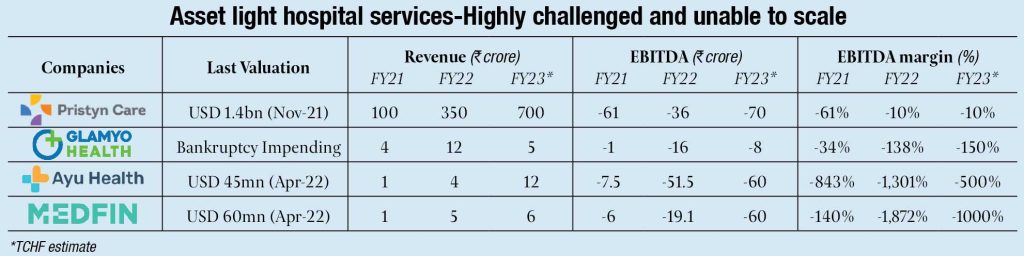

Asset Light Hospital Services

Highly challenged and unable to scale

- The Asset light hospital segment has received ~USD 200 million funding in last 2 years and have a cash runway of approx 6 months.

- The second largest player Glamyo Health is expected to file for bankruptcy due to financial mismanagement and inability to attract any fresh capital. The largest player, Pristyne Care has not raised any capital in the past 18 months and has missed its revenue targets consistently. The other players in the segment such as Ayu and Medfin remain sub-scale despite having raised ~ USD 50 million capital.

- The outlook for this segment is challenging and there could be a complete collapse as the demand side of the platforms requires gaining trust of patients for surgical procedures which is difficult over a digital platform as quality and familiarity with doctor is valued over speed and cost.

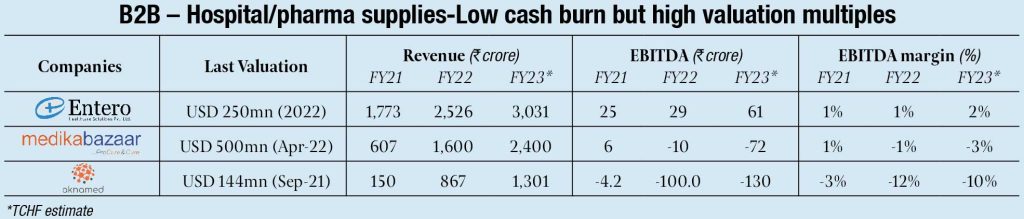

B2B – Hospital/Pharma Supplies

Low cash burn but high valuation multiples

- The B2B hospital supplies segment has attracted over USD 200 million private capital since 2015. The newer tech led hospital and pharma supplies procurement businesses are nearing profitability and cash-runway for the players is >12 months based as the burn in low (barring Aknamed – a PharmEasy company).

- The new age large players in the segment are profitable and continue to grow at >50 percent. Valuations in this segment have been expensive with transaction multiples ranging between 3x-5x EV/revenue, this could be a deterrent for new investor interest. Entero which is one of the largest player in the space is looking to launch its IPO in the next 12 months.

- We expect the segment to grow at >20 percent+ in the coming years as the shift from unorganized to organized gathers steam and existing players leverage inorganic growth strategy. Scale and operational efficiency will be the key to success in this segment as companies operate on thin margins.

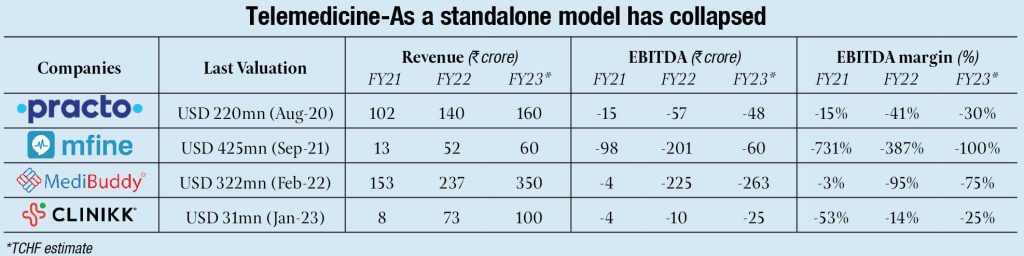

Telemedicine

As a standalone model has collapsed

- The sub-segment has seen funding of ~ USD 250 million over the past 3 years. Companies are operating on a very high cash-burn model and their current cash run-way is < 6 months.

- The sub-segment on a standalone basis has failed to establish a profitable model. Existing players like such as Practo, Medibuddy, Clinikk are generating majority of their revenues services like subscriptions, offline healthcare delivery (Clinikk has opened primary health centers), and diagnostic tests. Telemedicine has become a feature of a wider healthcare platform.

- This segment will actively scout for fresh capital given their limited cash run-way and unprofitable business model. We could see further disruption (employee lay-offs, discontinuation of services) and low growth rates by existing companies in this segment as the funding environment continues to be challenged.

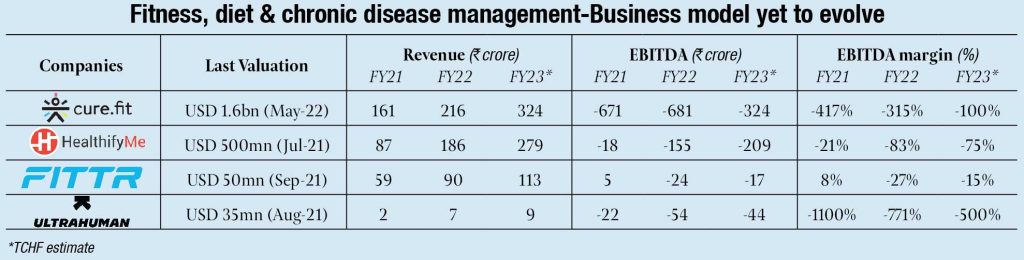

Fitness, Diet & Chronic Disease Management

Business model yet to evolve

- The sector has attracted USD 750 million in funding and despite unit economics for the space being well-established in the fitness and diet category, high cashburn has left the players with limited cash runway of < 9 months.

- The digital only players such as Healthify Me and Fittr are currently loss-making. The market leader Cure.fit backed by Tata Group is taking a phygital approach which has higher realizations and scale potential. Chronic Disease management sub-segment has faced scalability challenges, companies like Phablecare, Ultrahuman are unable to scale despite significant funding raised.

- The key to success in this segment remains the stickiness of the customer base as the value proposition and outcomes are well defined. In Chronic Disease management, the business models will continue to evolve as current models haven’t managed to scale.

Based on a Tata Capital Healthcare Fund report.