Industry

MedTech industry – A driving force for innovation and progress

In the coming years, as the MedTech industry matures, it will face both challenges and opportunities. As the makers continue to demonstrate their ability to provide superior clinical and financial outcomes, 2023 and beyond will remain the age of MedTech.

The Covid-19 outbreak brought to the fore two aspects – a properly functioning healthcare system is crucial, and global vaccination efforts demonstrated that industry can implement strong measures quickly when needed. Even though the pandemic has now become an endemic, the MedTech industry needs to invest in addressing urgent healthcare challenges, particularly unequal access and long wait times. The third industrial revolution, which is technology-focused, will play a significant role in this effort, with new advancements in screening, monitoring, diagnosis, and treatment. The use of artificial intelligence (AI), machine learning, and other digital technologies are enabling more accurate diagnosis and treatment, resulting in better patient outcomes. It also offers opportunities for the healthcare industry to improve the efficiency and effectiveness of healthcare services and to create new innovative solutions to address existing healthcare challenges. The industry must continue to work together with the government and academia to ensure that healthcare services are accessible to all and to improve the quality of care provided to patients.

Indian market dynamics

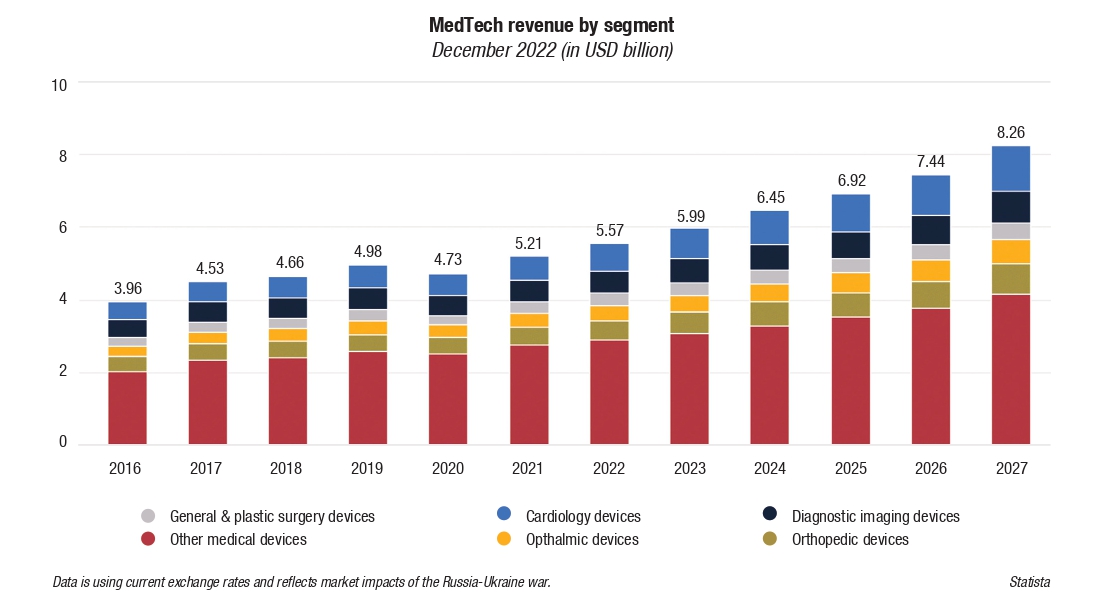

The Indian MedTech industry is poised for significant growth in the coming years, thanks to the support received from increased government focus, regulatory reforms, and technological advancements. According to the government data, there are 750–800 domestic medical devices manufacturers in India, with an average investment of USD 2.3–2.7 million and an average turnover of USD 6.2–6.9 million. Revenue is projected to reach USD 5.99 billion in 2023, and at an annual growth rate (CAGR 2023–2027) of 8.35 percent, in a market volume of USD 8.26 billion by 2027. In global comparison, most revenue will be generated in the United States (USD 163.70 billion in 2023).

One of the key drivers of growth in the Indian MedTech industry is the Indian government’s focus on improving healthcare access and outcomes. The government has implemented deep structural and sustained reforms to strengthen the healthcare sector and has introduced policies aimed at improving access to healthcare and promoting domestic manufacturing of medical devices. The government has introduced the Medical Devices (Amendment) Rules 2020 to boost the demand for medical devices in the market. The Department of Pharmaceuticals, Ministry of Chemicals and Fertilizers, Government of India, has presented an Approach Paper on Draft National Medical Devices Policy 2022 for consultation to drive the growth of the sector.

In addition, the Indian MedTech industry is benefiting from technological advancements, which are enabling the creation of new medical devices that are more effective, efficient, and affordable. With the growing patient demand and technological innovation, high growth can be expected in product areas, such as AI and machine learning-based medical wearables, robotics, and cloud-based remote patient-monitoring systems. AI is also facilitating the creation of increasingly sophisticated data-driven algorithms, such as autonomous diagnostics and prognostics.

Despite the recent Covid-19 holdups, opportunities thrive for MedTech companies of all sizes and maturity levels. The proposed policy strives to put in place a comprehensive set of measures for ensuring sustained growth and development of the MedTech sector, and address the further challenges of the sector, such as regulatory streamlining, skilling of human resources, lack of technology for high-end equipment, and lack of appropriate infrastructure, through a coherent policy framework.

The Indian MedTech industry is also benefiting from increased collaboration between industry players, stakeholders, and the government. KPMG, Invest India, and Asia-Pacific Medical Technology Association have proposed multiple recommendations, including predictable regulatory environment, harmonization of quality standards, a friendly public procurement policy, creation of supplier ecosystem and skilled talent pool, and establishment of Brand India as a global hub for medical devices manufacturing and innovation.

Despite the many opportunities for growth and development, the Indian MedTech industry still faces several challenges, including lack of appropriate infrastructure, inadequate funding, and lack of appropriate policies to promote innovation and research. These challenges must be addressed if the industry is to reach its full potential.

The future of the Indian MedTech industry looks bright, with significant growth expected in the coming years.

Global market dynamics

The global medical technology market will grow at a compound annual growth rate of 4.9 percent from 2023 to 2027. According to Deloitte, in 2023, this sector will be worth USD 465.5 billion and grow to USD 591.3 billion by 2027.

From a therapeutic segment standpoint, in-vitro diagnostics (IVD) remained the largest segment in 2022, generating nearly USD 134.07 billion or 21 percent of the total market. And while IVD is expected to decline over the next 3-year period to compensate for the high surge it underwent during the Covid-19 period, it will continue to remain the largest segment in 2025.

Despite the disruption caused by the pandemic, the global MedTech market has started to witness recovery, with certain categories showing higher growth than the others, depending on regulatory mandates and urgent medical conditions. Capital-intensive equipment like diagnostics are recovering at a slow pace, given the large budgets that are required. Device segments, such as ophthalmology, dental, cardiovascular, orthopedics, and general surgery are already showing signs of recovery and improved demand as the caseload increases.

Endoscopy, wound management, diabetes care, dental equipment and consumables, neurology, and general surgery devices markets are expected to deliver the highest growth to make up for the Covid-19-driven declines during the peak of the pandemic.

MedTech market trends

The medical device trends for 2023 aim to address current healthcare challenges. AI is being utilized to automate manual processes, workflows, and analyses for disease prevention and treatment. Cybersecurity is crucial in securing sensitive patient data and modern, wireless, and IoMT devices relied upon by healthcare systems.

Virtual technologies and medical robots are revolutionizing surgical procedures. Wearable devices are providing healthcare providers with real-time patient data remotely, enhancing patient engagement and outcomes. Here are some of the trends expected to have positive impact on MedTech industry in 2023 and ahead.

Uptick in self-diagnosing. Within the MedTech sector, there is an increasing emphasis on wellness – that is, getting people into a more health-conscious mindset by imparting knowledge through nudges in the right direction. The message central to this is that if small lifestyle changes are made today, they can have a major impact in the future.

Self-testing is set to become more common. During the pandemic, people across the globe incorporated lateral flow testing into their daily lives, and have become more accustomed to carrying out these self-tests. As a result, we are likely to see increased use of IVD (in-vitro diagnostic) testing, through blood or saliva, which can produce rapid results and help individuals to take more ownership of their health.

An advantage of this is greater awareness of one’s health, which may also help to reduce the pressure on health services, including GPs. We are seeing this already with wearable tech – namely smartwatches – providing information on heart rate, oxygen intake, caloric intake, and step count, which wearers can track themselves throughout the day.

Digital therapeutics. There is also likely to be further use of digital therapeutics (DTx), which is an evidence-based approach to managing patients’ disorders or diseases. DTx is software-based and uses digital inputs, such as mobile devices, apps, and the Internet of Things to provide bespoke health plans for each patient. This alleviates pressure on health services by enabling patients to manage symptoms themselves, leading to overall improvements in the quality of life.

An earlier example of this is the digital delivery of behavioral interventions to treat diabetes. A study conducted as many as 20 years ago found that interventions in diets and exercise levels early on could mitigate patients’ risk of developing Type-II diabetes.

Now, there is an increasing number of products being approved that allow patients to self-manage symptoms. Thanks to the innovation spurred on by the pandemic, I only see this increasing and given the pressure health services are under, this can only be good news.

More robust supply chains. The pandemic’s effects on health services have put the MedTech sector under increased pressure to meet the soaring demand. It laid bare supply chain vulnerabilities, as well as shortcomings in performance. Ultimately, this was a key learning for the sector.

The fact that these issues are now known, means that there is no excuse not to take action. If this does not happen, future waves of the pandemic and supply shocks could be devastating for these same supply chains. The sector must also consider other events, like cyberattacks, economic crises, and regulatory changes.

To ensure consistent quality and supply security, MedTech companies must assess and mitigate any vulnerabilities on an ongoing basis. This is especially important given the direct impact the sector has upon patient outcomes. These black swan events are difficult to predict but, given the nature in which the MedTech sector is regulated, preparation is vital.

Emphasizing inclusivity. In developing nations, health conditions typically progress further before patients receive treatment. This means that, while large developing markets, such as China and India, are fantastic opportunities for growth, whatever solutions are offered must be appropriate for the patient in that particular region. It means that just selling products/services that have been designed and tested for developed markets may not be appropriate.

Firms will also have to negotiate cultural challenges, such as language barriers. Frankly, it is as much about communication as it is about technology and medicine. At Nexus, we understand the need to go beyond STEM and use our global reach – thanks in part to our University of Leeds base – to do so.

There is also an issue of representation in data. Traditionally, medical devices were designed with white, middle-aged men, living in the developed world, in mind – this assumption of end-user must be challenged.

Thankfully, the industry culture has shifted to an evidence-based approach and takes the diversity of potential users into account. Adopting the one-size-fits-all attitude simply will not work here – just like with diseases, people react to different medical devices in a variety of ways.

Increased tech across the board. Various technologies are now playing a larger role in all areas of the sector. Virtual reality (VR) technology is improving product design capabilities and has also enhanced training processes. This means that trainees are receiving a higher quality of training, whilst time required to complete it is reduced.

Technology has also allowed companies to improve drug trials and help to speed up the time to market for new products. Mainly, they can now be conducted in silico trials via computer simulation. Not only does this mean greater efficiency but also the use of animals for testing purposes is no longer required – meaning companies can improve their operations and their ethics.

Challenges for the future

Although the pandemic did see some bureaucracy dismantled, there remain several regulatory challenges to contend with.

End of emergency use authorizations. With the Covid-19 public health emergency (PHE) set to expire on May 11, 2023, MedTech companies that brought devices to market under special pandemic rules will need to prepare transition plans soon. The expiration of the PHE has wide-ranging implications for healthcare industry leaders whose companies have operated in a more relaxed regulatory climate and benefited from an influx of government dollars intended to facilitate and support testing, vaccination, and care delivery throughout the pandemic.

Industry leaders should act now to verify that they are in compliance and have a game plan for a smooth transition for patients and staff when waivers lapse and certain pre-pandemic regulatory realities resume.

In comments responding to a draft version of the guidance shared in December 2022, MedTech companies and industry groups generally supported the transition period even as some asked for clarity on some specifics around labeling and the supply chain process.

Medical devices trade group, AdvaMed, supported the transition period but requested more flexibility with labeling changes, including letting manufacturers provide the information online, with the option for customers to request the updated labeling.

EU marketplace. In particular, the framework of regulation in the EU raises questions over what support is on offer to help start-ups to bring their products to market. Is there an opportunity to address some of this in the new UK MDR, which are due to come into force by mid-2024?

Of course, there have been notable exceptions to this – the severity of the pandemic required a break with convention to produce the required vaccines. However, this exceptional circumstance is exactly that – an exception – and it is still an ordeal to get products into EU markets. To compound this, the extra costs and red tape imposed by Brexit threaten the viability of many smaller innovative MedTech firms exporting to European markets.

Outlook

The MedTech industry is currently experiencing an era of rapid development, with new technologies and innovations emerging at an unprecedented rate. These developments have the potential to revolutionize the way one approaches healthcare, offering new tools and solutions that can greatly enhance their relationship with health. From wearables that monitor vital signs to AI-powered diagnostic tools, there is no shortage of exciting advancements that could vastly improve the quality of care patients receive.

However, even as these developments take shape, it is important to recognize that there are significant regulatory hurdles that must be overcome before many of these technologies can be widely adopted. From issues around data privacy and security to concerns about the safety and effectiveness of new medical devices, there are many factors that need to be carefully considered and addressed before new innovations can be fully realized. MedTech companies must work closely with regulators and industry experts to ensure that their products meet the necessary standards and that they are deployed in a way that is both safe and effective.

Beyond regulatory hurdles, there is also a pressing need for the MedTech industry to prioritize sustainability, if it is to continue to prosper in the future. From reducing the environmental impact of medical devices to addressing issues around the responsible use of resources, there are many areas where the industry can improve its relationship with sustainability. By prioritizing sustainable practices and taking a more holistic approach to product development, MedTech companies can help to ensure that their innovations have a positive impact on both patients and the planet.

If these issues can be effectively addressed, there is no doubt that the MedTech industry will continue to be a driving force for innovation and progress in the years to come. By embracing new technologies and working to create more sustainable and responsible products, the industry can help to transform the way we approach healthcare and improve outcomes for patients around the world. Ultimately, the key to unlocking the full potential of the MedTech industry lies in striking the right balance between innovation, regulation, and sustainability, and working collaboratively to create a brighter future for all.