MB Stories

Transforming uncertainty to opportunity

While globally biotech funding is going through a tough time, India seems to be defying the trends and is upbeat on this sector.

India is the third-largest destination for biotechnology in Asia, and one of the top 12 destinations for biotechnology worldwide. With biotechnology emerging as a sunrise sector in India, the country’s rise as a go-to destination for bioinnovation and biomanufacturing is a highly anticipated and sought-after outcome.

In 2021, India’s biotechnology industry reached USD 80.12 billion, growing 14 percent from USD 70.2 billion in 2020. It is currently estimated at USD 100 billion. The sector is likely to touch USD 150 billion in value by 2025 and exceed the USD 300 billion mark by 2030.

All major segments of the industry – biopharmaceuticals, bioagriculture, bioindustry, and bioIT and bioservices – are witnessing spectacular growth. The bioindustrial segment grew 202 percent in 2021 to USD 10.27 billion, driven by the government’s decision to focus on renewable energy. To this, biofuels contributed USD 5.97 billion, which is expected to increase to USD 20 billion by 2025, again almost tripling in size. With India’s biosimilars gaining a foothold in developed markets, such as the US, the biopharma sector is estimated at USD 63 billion in 2022, a growth of nearly 1.4 times. The bioservices and bioIT sector is predicted to nearly quadruple from USD 6.4 billion to USD 26.6 billion in 2025.

Foreign direct investment (FDI) in the Indian bioeconomy is estimated to have touched USD 830 million in 2021, an increase from USD 780 million in 2020. Nearly 49 percent of the Indian biotech sector is dominated by the pharma industry, while 18 percent related to Covid-related technologies, followed by the agriculture segment at 13 percent.

Diagnostics accounted for 52 percent of the pharma market in 2021, followed by the therapeutics segment with 26 percent, diagnostics and therapeutics together comprised over USD 30 billion of India’s bioeconomy.

The nation boasts around 5000 biotech companies, with more than 4000 being startups. This startup count is expected to reach 10,000 by 2024. The Department of Biotechnology (DBT) and the Biotechnology Industry Research Assistance Council (BIRAC) in India actively support and promote biotech startups through various funding opportunities. Their funding opportunities have been instrumental in supporting and nurturing innovation in the field. By providing grants, fellowships, and investments, DBT and BIRAC have helped researchers, startups, and institutions translate their ideas into impactful biotech products and solutions.

With a huge population of young and skilled workers, India has many ingredients for expanding the number of its biotech companies in the coming years. Add to this a large patient pool for lifestyle-related diseases, such as type-2 diabetes, and there is a large potential for generating innovations in healthcare.

The five largest companies today, going by those who raised impressive cash in the last few years, are Bugworks Research India Pvt. Ltd., Epigeneres Biotech Private Limited, Eyestem, Immuneel Therapeutics Private Limited, and MedGenome.

The industry does have mountains to climb

Inflation, depreciation of rupee, rise in the interest rates internationally, a slowdown in foreign economy because of which exports from India to these countries is affected, PLI scheme’s umbrella needs to be expanded to cover key aspects of biotech industry, and biotech suppliers are some of the headwinds that the industry is facing.

Currently, biotech companies cannot list on capital markets in India unless they are revenue-positive, which is impractical for the ecosystem. Thus, efforts need to be made to make Indian capital markets a practical option for such startups, which otherwise have to go to markets like Hong Kong, Singapore, and the US to access such capital.

Dependency on China for critical biological raw materials, such as amino acids, hydrocolloids, cofactors, enzymes, indicators, biochemicals, and fine chemicals needs to be addressed urgently with the support of government funding and other supportive policies. Economies of scale are very critical for us to be cost-effective, in-house, or local manufacturing of critical machine components, such as small pumps, chips, ready-to-use printed circuit boards (PCBs), etc., for the diagnostic and biopharma industries are the other major challenges.

The global market faces increased headwinds

Biotech funding environment has undergone significant changes in the last couple of years. Record-high levels of investment fell drastically, despite the availability of capital, creating more competitive markets that are spurring new approaches and perspectives within emerging biotech even as key funding players reshape the field.

Biotechs can no longer easily raise cash and quickly pivot to public markets before starting a clinical trial. Venture firms are now more focused on helping their existing portfolio companies survive in the tough financing environment. When they do back new companies, they are looking for safer bets and experienced teams.

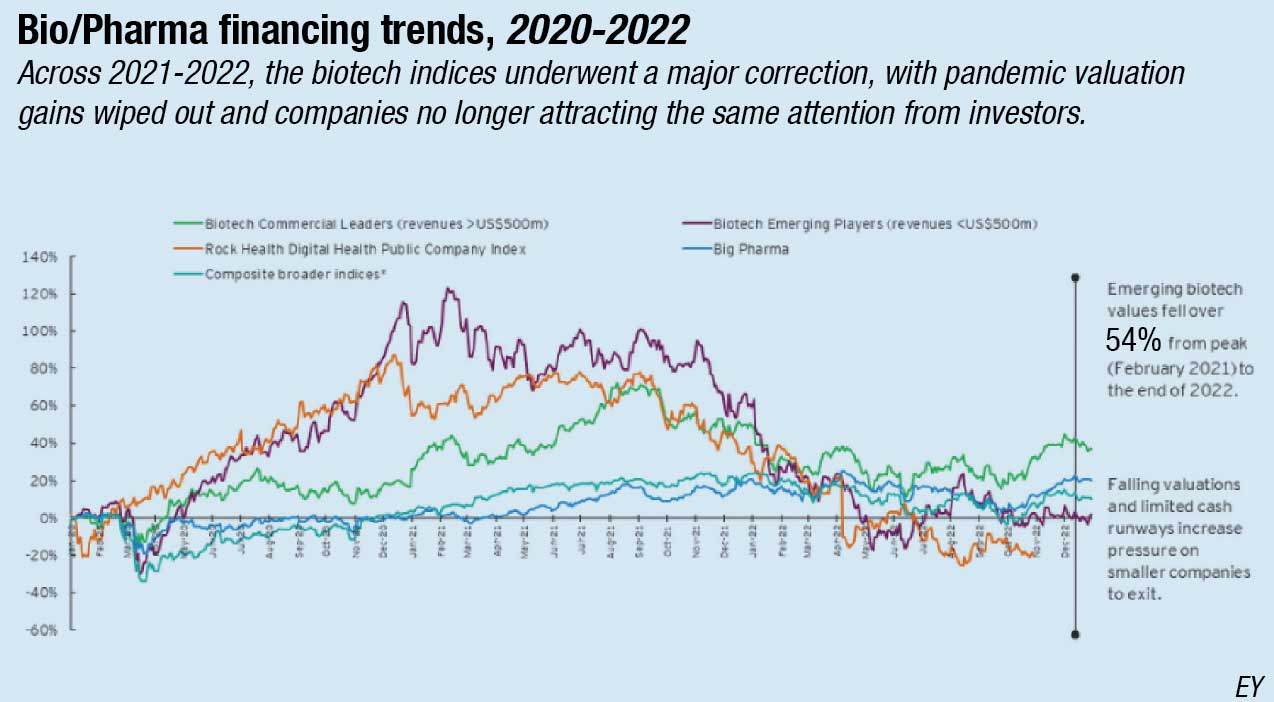

In fact, the party was over for biotech in 2022. The quick-flowing funds that were in the market in 2021, bottled up by 2022, resulting in fundraises that have – after two record-setting years – dipped 24 percent. The biotechnology sector’s funding environment had undergone significant changes in the last few years, demanding creative solutions in response. The record-highs of the bull market that gained critical mass through the late 2010s and early 2020s had stopped short. Interest rates were up and the once-hot biotech IPO market crashed, alongside its related model, the SPAC, effectively reducing capital and returns expected by Series A investors, market instability had shaken investors.

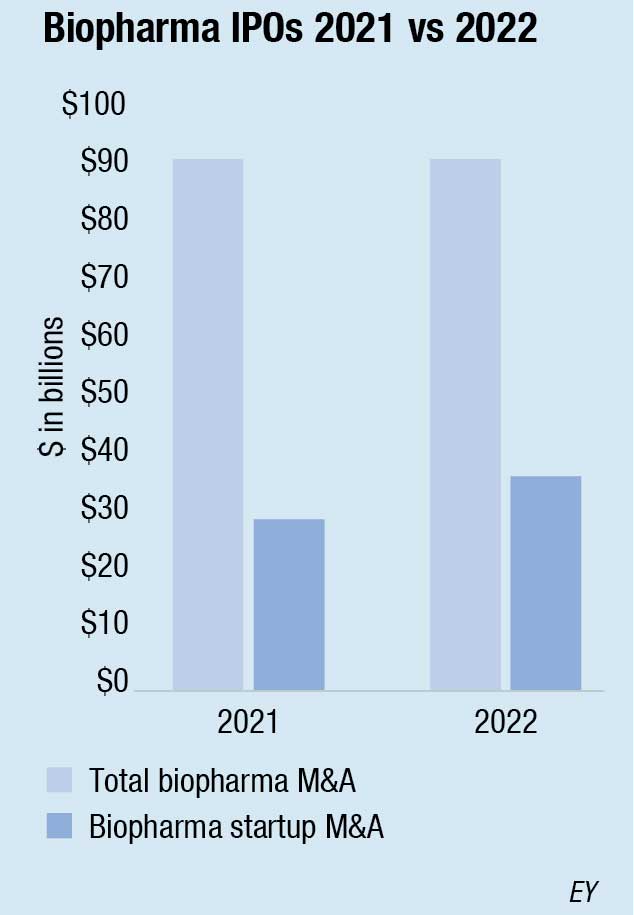

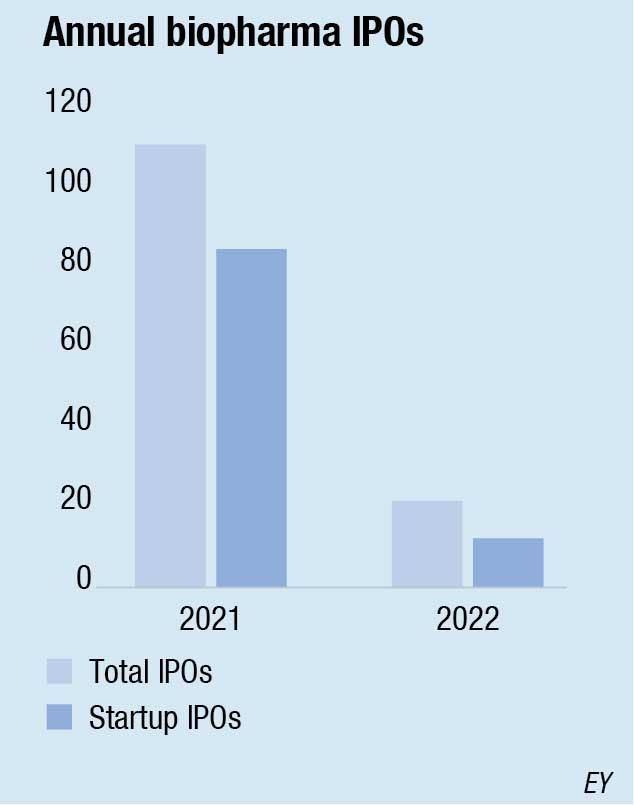

The first symptoms appeared in the United States as early as 2021. In the world’s largest biotech hub, only 18 American companies ventured to go public in 2022, compared with more than 70 in 2021, raising a total of USD 1.4 billion, the lowest level seen in 10 years. Investors became more discerning in their capital allocation strategy. After making capital gains, those who had invested in the sector at the beginning of the pandemic began to distance themselves. And, on the stock market, biotech valuations plummeted. IPOs followed suit.

The conservative financial climate translates into the need for creative deal structures as biotech companies continue developing their pipeline. As clinical trial data readouts can signal large value inflection points, deal structures to bridge to such a milestone are becoming more prevalent as companies cannot readily tap public markets. This can take the shape of innovative structures, such as selling royalties in exchange for trial services, tranched biotech debt facilities, and co-development with value-added partners.

There are more biotech companies now than ever before. Consequently, there is a large tranche of early-stage biotech in need of venture funding, precisely at a time when access to that funding has stifled. The funding market has become incredibly competitive, even in Series A, which has been the most stable, and traditionally last to be impacted by macroeconomic pressures, compared to late stage and crossover investments.

This lack of growth capital for many biotech companies means they must be very cautious in their spending, again resulting in pipeline culls and rounds of layoffs. In total, more than 100 biotech companies laid off employees in 2022, with more anticipated through 2023. Reprioritizing pipelines and optimizing development strategies will help biotech stretch their cash to advance their programs in the absence of additional capital investment.

Q1 2023 saw a remarkable shift as venture capital (VC) investors remained cautious toward biotech funding. VC investors put their money behind companies that can demonstrate a predictable development pathway with a proven commercial strategy, and thus can speak with confidence about the likelihood of a return on investment (ROI). They are more inclined toward companies focusing on protein, small molecule, and known platforms. These areas are comparatively proven, have shown consistent progress, and are more predictable in terms of development and commercialization cost.

HSBC’s data shows that in the first half of 2023, investors put USD 2 billion into 81 seed and Series A deals for biotech companies, pacing well below each of the last three years. Venture investment across the sector totaled USD 10.6 billion over 320 deals, numbers that are also lower than recent levels.

Arch Venture Partners was the most active venture firm in the first half of 2023, participating in seven deals, followed by RA Capital and Sofinnova Partners, according to the report.

Among the report’s other findings: While the most money went to cancer biotechs and platform companies, the amounts for each category fell and startups were also more advanced. Most oncology deals were Series B rounds or later, and 12 of the 20 largest involved companies are already in the clinic.

Notably, the three companies securing the largest rounds in the first half of 2023 – ElevateBio, ReNAgade Therapeutics, and Metagenomi – are involved in cell and gene therapy, a field in which many publicly traded companies are struggling to survive.

How biotech funding has dried up

To understand how biotech got where it is today, you have to rewind five years to when times were good, says Arda Ural, PhD EY Americas Industry Markets Leader, Health Sciences and Wellness.

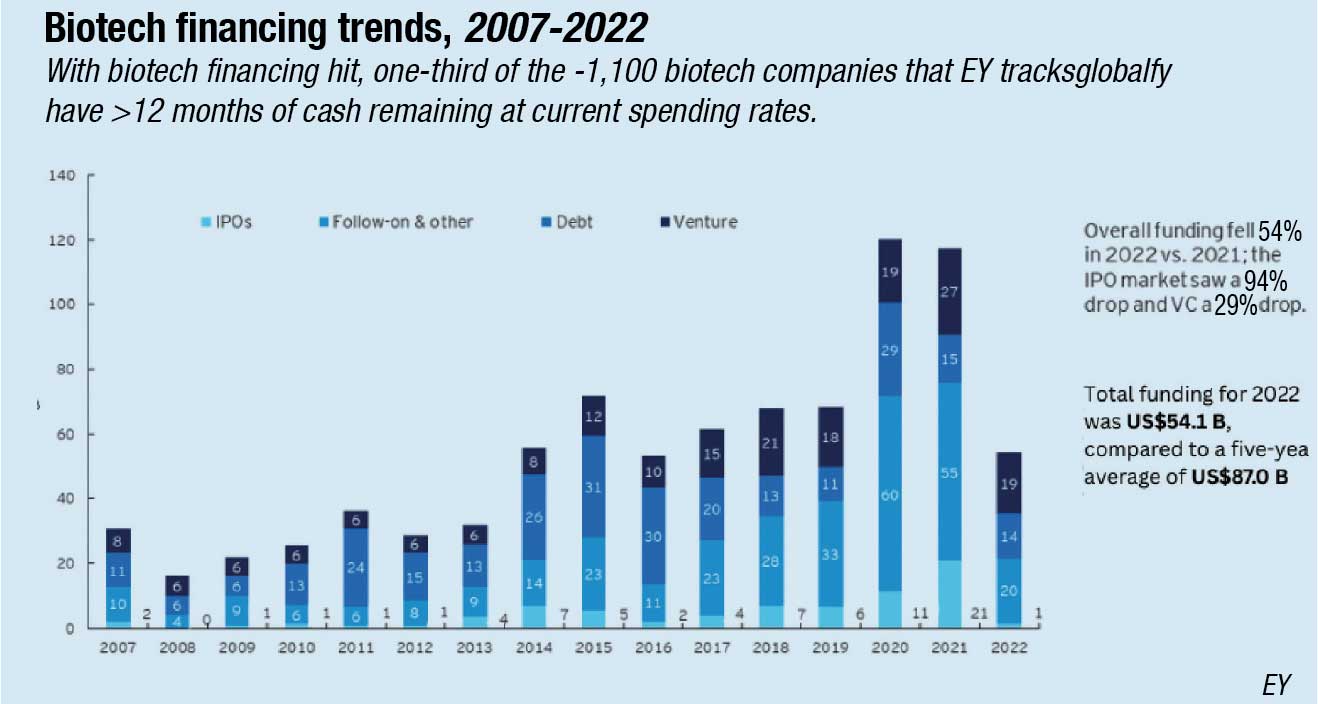

In 2018, there was an outsized number of biotech IPOs, with almost 70 biotech companies debuting on the public market, raising a total of USD 7 billion. It seemed as if any company – regardless of clinical data or corporate maturity – could execute an IPO. This was driven by the large venture capital (VC) funding rounds that seemed like they would never end. The VC numbers kept climbing as biotech valuations surged during the early stages of the Covid-19 crisis, and, in 2021, more than 160 biotechs completed IPOs, raising upwards of USD 20 billion.

This momentum came to a halt toward the end of 2021. Cross-sector funding started to fizzle out as investors from other industries became more cautious, and biotech valuations started to better reflect asset maturity and the availability of clinical trial data. Only 21 biotech companies made public offerings in 2022, and only five have sought to access the public market via this pathway as of April 2023. Overall, funding fell 54 percent in 2022 from the prior-year period, with VC funding also dropping 29 percent.

As more emphasis is once again placed on proof of concept, overall biotech valuations have dropped 30 percent. Those companies with assets in the preclinical phase and Phase-I are down 69 percent and 45 percent, respectively, as of January 2023. Prior to the recent biotech boom years, most companies were evaluated by the strength of their clinical trial data, which accrues as the asset matures. Those standards for investing were largely ignored during the recent boom years as companies with little to no trial data were able to garner large investments, based solely on promises. Those traditional standards for investment have returned, with companies that have late-stage, Phase-III assets showing valuations up 33 percent.

The recent failure of Silicon Valley Bank, which catered to a large number of biotech clients, showed just how little cash many biotechs actually have on hand (many small biotechs feared that they would not be able to make payroll before the government stepped in) and highlighted how little venture funding is currently available.

However, this restricted funding environment stands in contrast to the record levels of firepower – a company’s capacity to carry out M&A based on the strength of its balance sheet – that are available to the industry.

Beyond borders 2023

Biotechs are facing a complex path forward, says an EY report. They need to prioritize their capital allocation to navigate distressed public and capital markets, increased regulatory scrutiny, and macroeconomic disruptions. The good news is that the innovation capacity of the industry remains strong in the long term.

However, there are concerns over the long-term viability for the wider sector, as 55 percent of public biotechs (excluding companies with more than USD 500 million in annual revenue) hold insufficient cash to tide them over for the next two years. A further sobering fact is that 29 percent of these biotechs have less than a year of cash on hand. With venture funding falling 29 percent in 2022, and investors pursuing products that can deliver clinical or commercial validation sooner, companies are facing a constrained financing environment. In this instance, M&A remains a viable strategy for biotechs; dealmaking slightly increased last year compared with 2021 although the overall number of deals fell.

While challenges lie ahead for the industry, confidence can be found in the potential for a more efficient operating environment. This can be achieved by focusing on capital allocation strategies to secure future growth, optimizing tax management, building better financial and operational resilience, and utilizing artificial intelligence and other technologies to streamline commercial engagement models and more.

“The biotech sector should expect challenges and transformations in next few years as we prepare to scale the patent cliff,” said Rich Ramko, EY US Biotech Leader. “Biotechs must rev up their innovation engines to pull ahead in this race and put themselves into a position of strength. Companies that can produce differentiated products will set themselves up for steady revenue streams and more stability. All this can be achieved while focusing on operational efficiency and financial discipline.”

There is hope

Despite recent hardships in the industry, analysts are optimistic about the future. A surge in deal activity in the biotech sector is being predicted. This trend will be driven by the impending loss of market exclusivity for several major pharmaceutical companies within the next five years. As prominent drug developers seek to replenish their research and development (R&D) pipelines to offset exclusivity losses, it creates numerous partnership opportunities. The biotech industry stands ready for a period of increased collaboration as companies navigate the evolving landscape and leverage mutual strengths and resources.

July 2023 saw investors turn their attention to biotech. South San Francisco, California-based Septerna, closed a USD 150-million Series B, led by new investor RA Capital Management. Septerna focuses on small-molecule drugs that target G protein-coupled receptors, Founded just last year, the company has now raised USD 250 million. Cambridge, Massachusetts-based Crossbow Therapeutics joined the hit parade after raising a USD 80 million Series A funding round led by MPM BioImpact and Pfizer Ventures. The company is developing antibody therapies to treat a broad range of cancers. San Diego-based Arthrosi Therapeutics, a clinical-stage biotechnology company, closed a USD 75 million Series D led by Guangrun Health Industry. Founded in 2020, the company has raised more than USD 117 million.

That said, with multi-billion-dollar acquisitions on the horizon and ground-breaking innovations in drug discovery and technology, the global biotech industry appears to be poised for a comeback.